The Future of Small Business Lending

A Digital Experience + Vertical Specialization.

The COVID-19 pandemic has completely upended small business lending. Nearly 100,000 small businesses in the U.S. have permanently closed since the beginning of the pandemic. Banks and fintech companies — understandably nervous about lending in this environment — pivoted to distributing over $500 Billion in Paycheck Protection Program loans. Several of the largest fintech companies focused on small business lending — OnDeck and Kabbage — found exits.

All of which leaves us with a question — what does the future of small business lending look like?

Technology Isn’t Enough

For the purposes of this analysis, let’s assume we’re operating in a post-pandemic world where economic conditions for small businesses and lending conditions for banks and fintech companies have returned to some semblance of “normal”.

A lesson that I’ve learned from the last 15 years — since the emergence of online lenders like Lending Club, OnDeck, and Kabbage — is that technology can’t fully address the needs of small businesses.

Now, of course, those online lenders would disagree:

“At our very core, the focus has always been on automation and technology," Petralia [Kabbage co-founder and COO] says. "We ask the same exact questions that the banks ask, but we use data in a different way to get there faster."

They would argue that automation and data-driven underwriting dramatically lowers the costs of small business lending and enables them to profitably serve entrepreneurs that banks never could.

The pre-COVID data certainly supports the belief that small businesses will flock to the speed and certainty provided by such automation:

32% of small businesses applied for credit from online lenders in 2018, up from 24% in 2017 … Speed of decision making and perceived chance of funding were the top reasons firms applied to online lenders.

And yet, there’s a problem:

79% of small businesses that borrowed from small banks came away satisfied, compared to 67% for large banks and 49% for online lenders … Online lender applicants were most dissatisfied with high interest rates.

According to the data, small businesses are addicted to the speed and convenience offered by fintech lenders, despite the fact that loans made by those providers are generally worse for them financially.

Which tells me that technology alone cannot fully deliver the outcome that small business borrowers want — fast, convenient loans at fair prices.

Never Tell Me the Odds

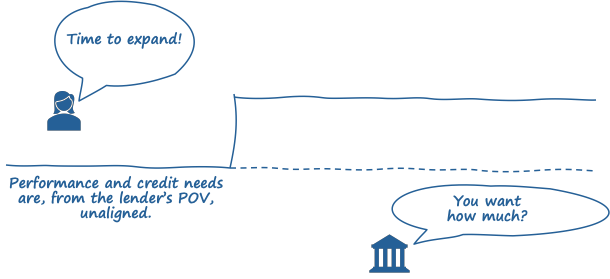

So how do we deliver that outcome? To answer that question, we first need to answer a related question — why is pricing risk in small business lending so hard?

What is it about lending to small businesses, specifically, that makes big banks so conservative in their approval rates (small business owners view big banks as least likely to approve them for loans according to SBA data) and fintechs so excessive in their loan pricing?

The answer is simple — starting a small business is irrational.

Half of small businesses fail within five years. 70% within ten years. To start a small business requires a Han Solo-ian level of confidence.

At a societal level, this type of confidence and ambition is critical. Our economy is built on it. In many ways it’s the purest expression of the American Dream.

But at a risk management level, it often looks utterly insane.

The Difference Between Data and Understanding

Here’s a quick example.

Let’s say we have an investment banker, living in Santa Fe, who hates her job. As a hobby, she starts making donuts on the weekends. Her friends love her donuts so much that word starts spreading and soon she’s being asked to cater a few weddings and birthday parties. She does so out of her house, using the equipment she already has, and making enough money to pay for her expenses and keep a little extra. At this point, the financial performance of her “business” (modest) matches her credit needs (nonexistent).

Then, with ample encouragement from her friends, she decides to quit her job as an investment banker and start a full-time donut business — Port-hole-io (sorry). Her first order of business is buying two industrial fryers and an industrial oven — a $20,000 capital expenditure — for which she seeks a loan from her bank.

And here we hit our problem. Our investment banker-turned-baker’s ambition, while perfectly rational to her based on her personal experiences, looks irrational from her bank’s perspective. The available data — cashflow, business history, collateral — doesn’t justify the risk.

What’s needed, to bridge this gap, is understanding; the ability to analyze the available data (requested loan amount, cashflow, business history, collateral) within the context of the business opportunity that the entrepreneur is so passionately pursuing.

This is why, in spite of their technology deficiencies, community banks are actually pretty good at small business lending and why small business owners are most satisfied working with them. They analyze data within the context of the opportunity — can a new donut business succeed in Santa Fe? Their knowledge of the community (and the local donut scene) helps build a bridge between the their risk management worldview and the investment banker-turned-baker’s entrepreneurial worldview.

Small Businesses Are Like Early-Stage Startups

The concept of ‘understanding’ as a risk evaluation tool in a data-deficient environment isn’t radical nor is it new to the world of entrepreneurship.

In venture capital investing, it’s called vertical specialization. Here’s Ali Hamed at CoVenture on why vertical specialization in VC investing can be advantageous:

It allows you to invest in a company before there is data that validates the company is on to something. … When I see a deal in a space I know well… like in lending — I don’t have to wait for the company to have customer data before making an equity investment. I have seen so many companies in the space that I know what default rates will probably look like, costs of origination, servicing, collections, and whether or not borrowers will take the money. I know if the company will be able to access debt capital markets.

The Ideal Small Business Lender

So what does the ideal small business lender look like? In my opinion, there are two primary criteria:

Ability to deliver a streamlined digital lending experience.

Vertical specialization.

Most big banks and the current generation of fintech lenders excel at digital, but aren’t structurally well-suited for specialization. Community banks struggle mightily with delivering streamlined digital experiences and their specialization is rooted in geography rather than industry expertise.

What’s really needed is a fintech company that is hyper-focused on a specific vertical.

Something like Karat:

Karat’s first product is the Karat Black Card, designed specifically for influencers, with credit lines starting at $50,000. Its perks can be customized (gamers get cash back on streaming services; beauty influencers get perks for product purchases), and the credit limits are determined by an influencer’s social metrics, revenue streams, and cash in hand.

The influencer market is big and growing quickly:

The influencer market will be, by some estimates, worth close to $15 billion in just a few years, with hundreds of thousands of people earning sizable income from viral videos and social posts. By Karat’s own count, there are over a million professional full-time creators globally who earn at least $80,000 a year

And Karat’s cofounders — Eric Wei and Will Kim — evince a deep and nuanced understanding of it (Eric Wei worked at Instagram):

Each social media platform has different options for monetizing an audience, and some are more lucrative than others. “I’d rather have a million followers on YouTube than 10 million on TikTok,” says Wei, since YouTubers can get money from both ad revenue and channel subscriptions, while TikTok has no direct monetization options and makes it difficult to follow specific creators. Engagement is also critical. An influencer with 1 million followers and 10 percent engagement will do better than another with 10 million followers and 1 percent engagement, because engagement doesn’t scale linearly. In gauging creditworthiness, Karat also looks for signals that the creator has “professionalized” (incorporating their business, responding to emails on time) and the ways they have diversified their revenue (affiliate links, AdSense, sponsorships, subscriptions, and merchandising). It’s essential to see that they’re not mono-platform, Kim says, since “creators who are too reliant on any one platform struggle when something goes wrong with that platform.”

The Embedded Finance Advantage

As bullish as I am on Karat conceptually, it will face the same challenge that every B2C fintech startup faces — acquiring customers in a crowded market.

You know who won’t have that problem? Toast, a restaurant technology provider based out of Boston:

Toast has launched Toast Capital so its customers can secure loans, with restaurant-specific quirks in mind, like “seasonality and restaurant profit margins,” according to Tim Barash, chief financial officer at Toast. Toast will offer loans between $5,000 to $250,000 to restaurants that already work within the Toast network

Like Karat, Toast evinces a deep understanding of the unique challenges of running a restaurant and how those challenges should influence loan product design:

if a restaurant brings in, say, $5,000 on a Monday, but on Tuesday it brings in $10,000, the restaurant “will pay less on the day they made less.” So it’s a model where you pay a percentage of what you make each day.

Unlike Karat, Toast already has a large customer base to cross-sell its new loans to, which will significantly lower its acquisition costs. And as Andreessen Horowitz points out, vertical-specific software companies tend to have especially large and receptive customer bases:

the vertical SaaS business that can best serve the needs of a specific industry often becomes the dominant vertical solution and can sell both software and financial solutions to their core customer base.

With the growing maturity of fintech infrastructure and banking-as-a-service providers, I anticipate that the next decade of small business lending will be dominated by niche fintech startups and vertical-specific B2B service providers.

Good news for our hypothetical investment banker-turned-baker.

Short Takes

(Sourced from This Week in Fintech)

Chasing After Kids

Chase introduced a new bank account for kids (and their parents), focused on building healthy financial habits, powered by Greenlight.

Short take: Debit cards for kids is suddenly quite a crowded field, but Chase’s participation will elevate the concept to a new level. I’m a fan. The days of your parents sitting you down and showing you how to write a check are over. We need new ways to teach kids about the mechanics of financial services.

Employees Are People Too

PayPal CEO Dan Schulman commissioned a study and found that more than 10,000 people inside of PayPal struggle to make ends meet. He is working to change that.

Short take: It’s baffling to me why more financial services companies don’t invest in their employees’ financial health. A.) it’s the right thing to do. B.) it’s the profitable thing to do (PayPal’s investments in financial health have decreased employee attrition). And C.) it gives you an opportunity to experiment with financial health services that can then be extended to customers.

Double Secret Investment

Standard Chartered's fintech investment unit has made an undisclosed investment in passwordless authentication outfit Secret Double Octopus.

Short take: Passwordless multi-factor authentication is cool and definitely needed (passwords have long been recognized as a major weak link in corporate information security), but honestly I just wanted to write the name ‘Secret Double Octopus’ in my newsletter and point out how similar its logo is to SPECTRE’s logo in the James Bond franchise.

Thanks,

Alex Johnson