The Secret to Spinning Off a Digital Bank

It's easy (and yet really hard) — only swing at the right pitches.

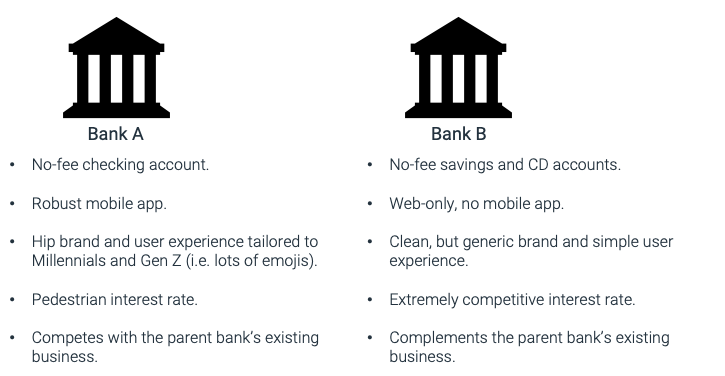

Compare these two digital bank spinoffs:

Now, if you were forced to guess, which one would you say has been more successful?

Bank A, right?

That’s the obvious answer. Bank A is following the consensus digital transformation blueprint — a willingness to disrupt its existing business with a checking account built on top of a robust mobile app with a hip, Millennial/Gen Z-focused brand.

By contrast, Bank B seems like it hasn’t been paying attention. Savings accounts and CDs, really? People don’t care about saving! A comparatively boring brand? How will you stand out from the crowd? And no mobile app? Insane!

The obvious answer is wrong.

Bank A is Finn, by JPMorgan Chase, which was shut down after a year with little to show for it. Bank B is Marcus, by Goldman Sachs, which has gathered $60 billion in deposits in the U.S. and UK since 2016.

Both digital spinoffs were launched around the same time. Both were launched by large, sophisticated companies with deep pockets and bank charters. But one succeeded wildly and one failed spectacularly. Why?

Substance Over Style

To answer that question, it’s useful to reach for an analogy. Baseball — as it often does in matters of strategy — provides the best one.

Ted Williams famously wrote:

A man has to have goals - for a day, for a lifetime - and that was mine, to have people say, 'There goes Ted Williams, the greatest hitter who ever lived.

By many statistical measures, the left fielder for the Boston Red Sox succeeded.

He was a six-time American League batting champion, a two-time Triple Crown winner, and he finished his playing career with a .344 batting average, 521 home runs, and a .482 on-base percentage, the highest of all time.

His 1941 season is often considered to be the best offensive season of all time, with a .406 batting average that was the highest batting average in the major leagues since 1924, and the last time any major league player has hit over .400 for a season after averaging at least 3.1 plate appearances per game.

So, how did he do it?

The answer is deceptively simple — he never swung at a bad pitch.

Williams wasn’t the flashiest player. He was famously standoffish with fans and the press. He didn’t play in as many all-star games as Willie Mays or win as many MVP awards as Joe DiMaggio (who beat him out for the MVP in his all-time great 1941 season).

But Williams studied the art and science of hitting a baseball with a fanaticism that has never been equaled. Here’s his replacement in left field, Carl Yastrzemski:

He studied hitting the way a broker studies the stock market, and could spot at a glance mistakes that others couldn't see in a week.

Long before Sabermetrics and Moneyball, Ted Williams had mapped out his strike zone as a grid of baseballs, 7 wide by 11 high, and calculated the exact percentage he knew he could hit for each ball.

Seriously, look at this:

Combined with great eyes, a quick swing, and an amazing level of discipline at the plate, Williams leveraged his understanding of his own abilities to set records and terrify opposing pitchers. Here’s American League MVP pitcher Bobby Shantz:

Did they tell me how to pitch to Williams? Sure they did. It was great advice, very encouraging. They said he had no weakness, won't swing at a bad ball, has the best eyes in the business, and can kill you with one swing. He won't hit anything bad, but don't give him anything good.

Lessons for Spinning Off a Digital Bank

So, what lessons can banks take from the story of Ted Williams and the success and failure of Marcus and Finn respectively, when contemplating a digital spinoff?

Know thyself. Despite the pleas made by fintech observers like myself, most banks aren’t interested in proactively disrupting their existing businesses. That’s OK! Goldman Sachs and JPMorgan Chase were both unwilling to cannibalize their existing revenue streams with their new digital initiatives. The difference is that Goldman knew that going in and picked a complementary market to go after with Marcus first. Chase tried to split the difference with Finn by targeting the retail banking market, but not allowing anyone living in close proximity to a Chase branch to open an account.

As I’m sure Ted Williams would agree, a half-hearted swing is much worse than no swing at all.

Focus on value. In baseball, home runs are sexy, but on-base percentage is arguably more valuable for winning games (for reference, Ted Williams is tied for 20th in career home runs, but is 1st in career on-base percentage).

In banking, mobile apps are sexy, but the success of Marcus (which didn’t have a mobile app for its first three years) demonstrates that it’s not essential for building a strong consumer value proposition. Finn could not have been more transparent in its attempt to appeal to young adults, but it’s Marcus that has succeeded in attracting the most desirable young adults (Millennials who make over $100,000 a year) to its platform, based on a survey on it’s forthcoming checking product conducted by Cornerstone Advisors.

Don’t be discouraged by short-term failures. According to Ted Williams, “Baseball is the only field of endeavor where a man can succeed three times out of ten and be considered a good performer.”

Related: Marcus lost $1.3 billion between 2016 and 2019, according to reporting from the Wall Street Journal. Not terribly surprising when you consider the costs of standing up a multi-product retail bank from scratch. According to the WSJ, the credit card they built with Apple cost $300 million. And the acquisition of Clarity Money (built by the same team that eventually built the Marcus mobile app) reportedly cost another $100 million.

What is notable is that despite the money lost, Goldman Sachs has remained disciplined in the slow, but steady expansion of Marcus — going from savings in 2016 to personal lending and credit card by the end of 2019 (with plans for checking and wealth management products by 2021).

Fueling this patient approach to growth and tolerance for short-term losses is an understanding that the odds are ultimately on its side. Marcus can offer significantly better deposit rates than traditional banks because, according to Harit Talwar, “we don’t have any legacy costs.” Those deposits then drive cost savings for the broader organization, according to Goldman Sachs’ CFO Steven Scherr, “for every $10 billion in new deposits, Goldman can reduce the cost of capital by $80 million.”

Swing at the Right Pitches

There has been plenty of digital ink spilled on the wisdom of traditional banks spinning off digital pure plays. What Marcus and Finn demonstrate is that the success of a digital spinoff strategy hinges on the discipline to only swing at the right pitches.

Thanks,

Alex Johnson