Blend's Big Bets

Breaking down the fintech infrastructure company's S-1.

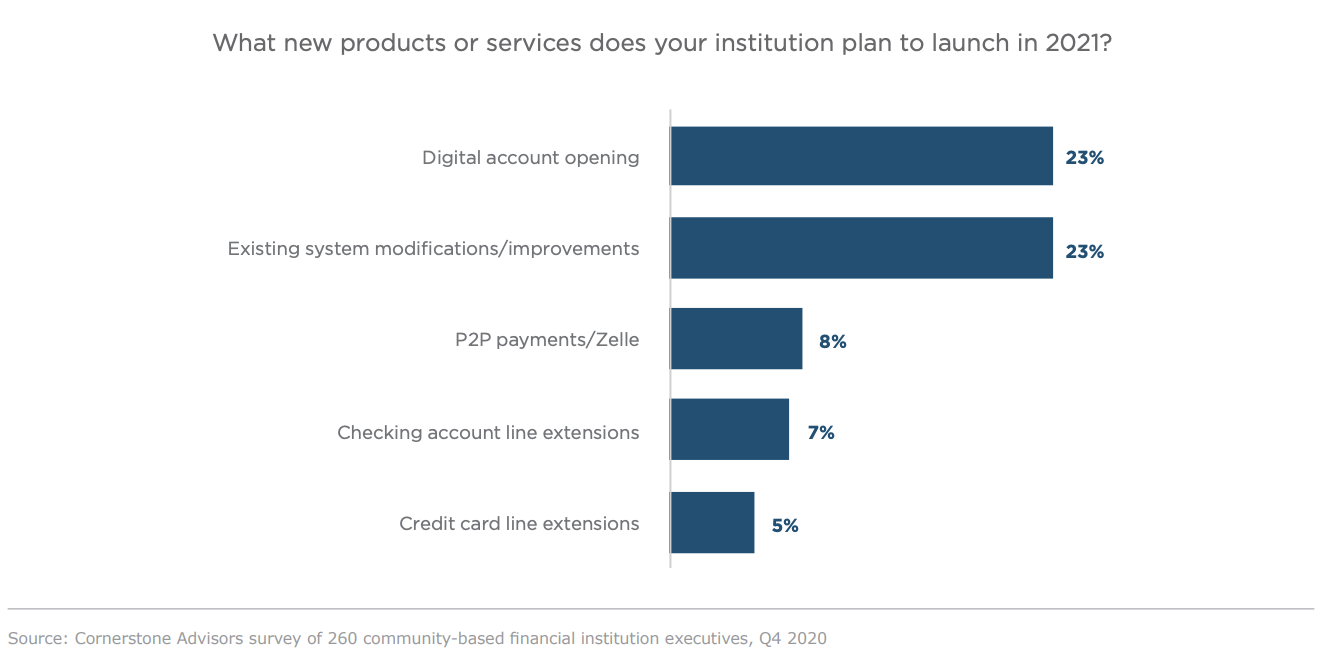

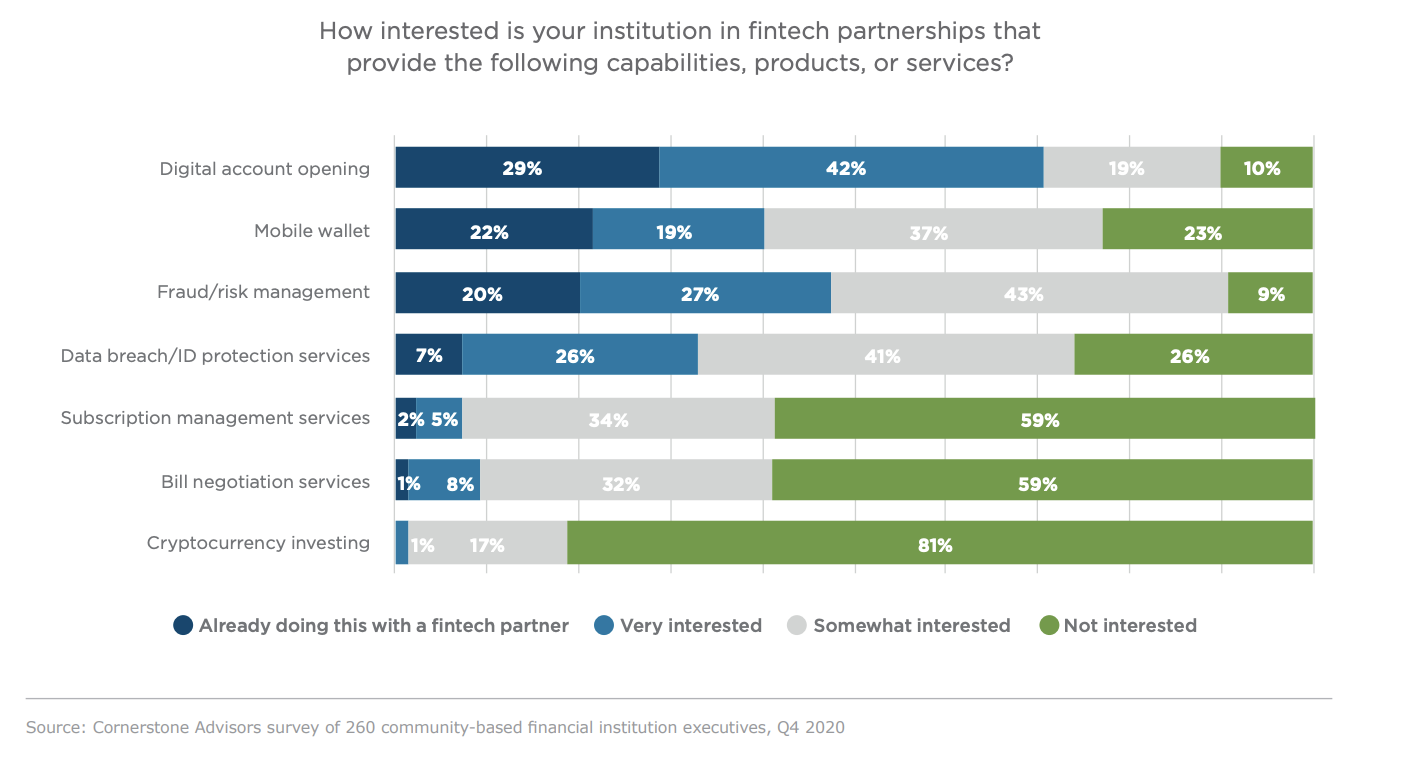

Banks have an unhealthy obsession with digital account opening.

It consistently ranks number one when bank executives are asked “what technology are you planning to buy or replace?”

It ranked number one when those executives were asked “what new products and services are you planning to launch this year?”

It even ranked number one when they were asked “what are your priorities for fintech partnerships this year?”

I’d be willing to bet that if we asked bank executives “do you believe that fintech companies have a magic power and, if so, what is it?” a majority would answer “yes” and “digital account opening.”

Small wonder then that an entire category of fintech infrastructure companies — including Amount, nCino, and Blend — have emerged in recent years to help banks apply that ‘fintech magic’ to the task of transmuting their leaden, paper-based account opening processes into the shiny, digital-native experiences that they desperately desire.

But how big, exactly, is that market opportunity? And how much of it can any one fintech infrastructure company capture? And how else might those fintech companies try to grow if Plan A doesn’t pan out?1

I’ve been wondering about these questions for a while and I figured the upcoming Blend IPO (and the corresponding S-1, which just dropped) would be a good excuse to dig in.

What is Blend?

Here’s a lede that would make any fintech PR firm faint with joy (emphasis mine):

By the end of last year, 13.6 million mortgages worth $4.3 trillion had been closed, shattering the previous all-time record of $3.7 trillion in 2003. It was a miraculous feat, considering that most of that lending was done while in-person meetings were taboo and overworked loan officers operated from ad hoc home offices as their dogs barked and children fidgeted through remote classes.

Truth is, the mortgage market probably would have melted down were it not for a secret weapon: Nima Ghamsari, a 35-year-old Iranian immigrant who made hundreds of thousands of dollars playing poker online while at Stanford; joined secretive big-data startup Palantir Technologies upon graduation; and then, at just 26, quit that dream job to start his own software company, Blend Labs, in 2012. “I have always felt like I wanted to bet on myself. I’m willing to take a lot of risk,” he says matter-of-factly.

The references to Mr. Ghamsari’s poker playing past and his comfort with taking risks might appear to be simple rhetorical flourishes except that the more you study the company he co-founded, the more it becomes clear that making high-risk bets is very much a part of Blend’s DNA.

We’ll review a couple of those bets later, but first a few pieces of background information on Blend:

Blend is a provider of digital lending and account opening technology, focused on helping incumbent financial institutions digitally transform themselves in order to better compete with fintech companies and other non-bank lenders. It provides digital infrastructure to 280+ U.S. banks, which include 31 of the top 100 U.S. banks by assets under management.

As referenced in the quote above, Blend specializes in digitizing the end-to-end mortgage loan origination process, from acquisition through closing. This was a particularly good business to be in over the last 18 months, with Blend’s software processing $1.4 trillion in mortgages in 2020, which was roughly a third of the overall market and a nearly 3x increase (for Blend) from 2019. The primary value provided by Blend’s software is efficiency. According to an analysis done by MarketWise Advisors, Blend saves an average of 7.3 days and $520 in operational costs per loan and allows a typical banker to close 14 mortgages a month. In real world terms, this manifests as results like what U.S. Bank saw in 2020 — a 136% increase in mortgage fee revenue with no increase staff.

On the financials front, Blend generated $96 million in revenue in 2020, a roughly 90% year-over-year increase from the $50 million generated in 2019. 53% of that $96 million generated in 2020 came from just 18 customers, a level of concentration that is both a concern and not at all unusual for fintech companies at this stage (see Marqeta and Affirm). Net losses for Blend in 2020 were $76 million, with a growing percentage of expenses going towards staffing (750 employees, up from 425 before the pandemic). Blend raised a $300 million Series G at a $3.3 billion valuation in January, doubling its valuation in a span of just five months.

Let’s take that $3.3 billion valuation as a baseline and assume that Blend’s ambition is to exceed it. How might that happen? What are the specific growth strategies that Blend will pursue in order to realize its lofty vision to “bring simplicity and transparency to financial services, so everyone can gain access to the capital they need to lead better lives”?

This brings us back to the bets that Blend is making (and selling to investors in the lead up to its IPO). By my reading of the S-1, there are two primary wagers that Blend is making on how it can continue to accelerate its growth as a public company. I’ll review both bets below, with some commentary on the potential upside (if things work out the way Blend believes they will) and the reasons why they are risky (note - these will bear little resemblance to the risk factors outlined in the S-1, which were written by lawyers and aren’t especially interesting).

Blend’s Big Bets

Become the digital rebundling engine of consumer banking.

The bet: While it’s almost exclusively operating in the mortgage space today, Blend believes that it has built a generic decisioning, workflow, and case management platform that is capable of facilitating streamlined, digital-first account opening experiences for any banking product:

Our software platform powers the mission-critical interface between financial services firms and consumers. Our growing suite of out-of-the-box, white-label products currently powers digital-first consumer journeys for mortgages, home equity loans and lines of credit, vehicle loans, personal loans, credit cards, and deposit accounts. Each of our out-of-the-box products is built from an extensive library of modular components assembled into consumer journeys that typically include data collection, verification checks, product selection, pricing, pre-approvals, disclosures, addressing stipulations, and signing closing documents. Through our low-code, drag-and-drop design tools, we also enable the creation and deployment of new product offerings. While we currently offer products for consumer banking, we plan to extend our modular software platform over time to add support for commercial banking products.

Blend believes that, collectively, the market for digital account opening across all lines of business is massive:

We currently estimate the serviceable addressable market for Blend to be greater than $33 billion, based on the number of home financing and consumer banking transactions in the United States

Most importantly, Blend believes that consumers prefer the convenience of getting all their financial products and services from a single provider:

Consumers prefer simplicity and convenience when it comes to shopping for financial services. Fifty-three percent of consumers would like to be offered bundled products, such as real estate services with a home loan or car deals with a pre-approved auto loan. To retain consumers and drive incremental revenue, financial services firms need to provide end-to-end consumer journeys that include these elements.

And that its technology (when used across all of a bank’s LOBs) can effectively facilitate these rebundling and cross-sell strategies:

we increase loyalty and lifetime value for our customers by allowing consumers to explore multiple product offers in a single session. For example, consumers can complete a mortgage application and be presented with an immediate opportunity to open a deposit account or apply for a credit card without having to re-enter information.

we support multi-product shopping experiences and enable consumers to move seamlessly across digital devices, contact centers, and branches throughout the origination process, providing additional benefits and incentives for customers to standardize on our software platform across products and channels.

If it works: Blend is betting that the future of financial services looks, structurally, a lot like the past — a small number of financial institutions (likely a mix of existing incumbents and challenger banks that reach massive scale) all offering a broad suite of products and services that they cross-sell customers into over time using thoughtfully-designed bundles and conveniently-integrated experiences.

In this future, Blend would have the opportunity to act as a massive ‘rebundling engine’, facilitating the continuous development and cross-sell of new digital financial products and services for market leaders and aspiring disruptors alike, which, as Simon Taylor recently wrote, would allow them to “essentially become an index stock on the rise and fall of the US lending market (except with software unit economics).”

Why it’s risky: There are a couple of concerns worth elaborating on:

First, and most importantly, it’s possible (verging on likely) that the financial industry of the future ends up looking, structurally, quite different from the past (and the present). Blend is assuming that the current unbundling of financial services will eventually give way to a period of rebundling because, all things being equal, consumers always prefer the convenience and low cost of getting multiple products from a single provider.

The flaw in that assumption is that financial products aren’t like other products.2 People don’t actually want them; they want the things that they can get with them. As Blend itself is fond of saying, “no one wants a mortgage — they want to buy a home.” Given this and given that the ‘atomization of banking’ has enabled any company to offer financial products and services, there’s no reason to believe that a consumer 10 years from now will prefer to get a mortgage, a checking account, and a credit card all from the same bank instead of getting a mortgage from Zillow, a checking account from their employer, and 12 different BNPL loans from their favorite 12 merchants.

Second, despite Blend’s optimism and the hundreds of millions of dollars in VC money that it can throw at product R&D, it will be extremely difficult to build and sell best-in-class digital account opening solutions for every line of business in banking.

One of Blend’s key operating principles is building software that delivers 10X better consumer experiences. Blend has undoubtedly achieved that in mortgage — a line of business that it knows extraordinarily well and that legacy solutions leave plenty of room for improvement in. However, other lines of business will prove trickier to realize that 10X better lift in. Account opening for checking accounts, credit cards, and personal loans are already highly digitized (at least among the big banks) and auto loans are largely originated through indirect channels which constrains the experience improvements that any technology vendor can introduce.

Additionally, there are serious competitive threats that will put pressure on Blend as it attempts to build out its non-mortgage business. Amount specializes in personal lending (coming from its Avant roots) and increasingly in BNPL. nCino (which already made its public market debut a year ago) is the dominant provider in the commercial banking space and is rapidly moving into consumer banking products. And a whole raft of legacy technology vendors — Experian, Zoot, Provenir, CRIF, FICO, etc. — will continue to make their presence felt.

Monetize an unprecedented, multi-sided platform for home buying.

The bet: Every vendor in the loan origination and account opening space brags about their partner ecosystem. Usually this is just a fancy way of dressing up the pre-built integrations that these vendors have with other vendors to facilitate access to needed third-party products and services like credit data and KYC. The number of partners in a typical vendor’s ecosystem is usually numbered in the dozens.

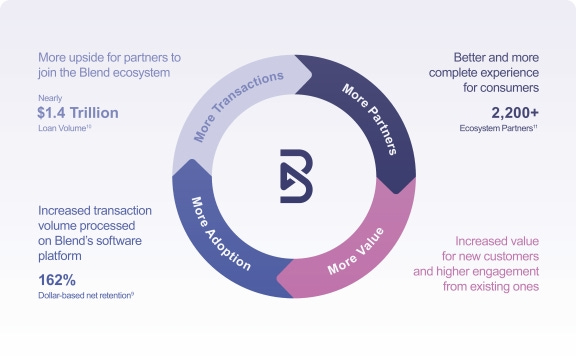

Blend has built an ecosystem of 2,200 active partners.

That’s staggering. Especially so when you consider that only a minority of them are the typical data and technology partners that other vendors refer to when discussing their ecosystems.

So, who are the majority of Blend’s ecosystem partners and why has the company dedicated an unusual amount of resources to building and maintaining them?3

I’ll let Blend answer:

As consumers use our software platform to apply for financial services products, they can shop for realtors, insurance carriers, and other service providers through integrated marketplaces that are introduced at the precise moment these third parties are needed. As more consumers use our software platform, we are able to attract a broader range of ecosystem partners, which allows us to deliver more value to consumers and attract more financial services firms as customers. This creates a powerful network effect and differentiator for our business. As of March 31, 2021, the number of participants in our ecosystem has grown by more than 1,300% year-over-year.

Put simply, Blend is aggregating the demand of all of its bank customers’ end customers (consumers applying for mortgages), matching up those consumers up with relevant third-party service providers, and collecting a small referral fee each time.

This is a highly efficient approach for building a lead aggregation business, as Blend notes:

By providing the software that powers consumer journeys at financial services firms across digital, contact center, and branch channels, we are able to benefit from a substantial volume of high-intent consumer traffic with no incremental acquisition costs.

And while it hasn’t been deeply monetized yet, it will be:

Although we have generated an immaterial amount of revenue through commissions or service fees when consumers use our marketplaces to select a real estate agent, property and casualty insurance carrier, or title and settlement services entity in 2020, we expect this will become a significant part of our business in the future.

If it works: As a reminder, Blend’s software processed $1.4 trillion in mortgages in 2020. That was roughly one third of the entire U.S. mortgage origination market that year. Normally these kind of aggregated stats are empty boasts, a way of directly comparing backend infrastructure providers to their better-known B2C counterparts (Look! Blend is actually bigger than Rocket Mortgage! Isn’t that cool?)

Except in this case it’s not an empty boast. Blend is building a lead aggregation business on top of its digital lending technology business and that digital lending technology business originated more than four times the volume of mortgages that Rocket Mortgage originated in 2020!

Even with modest growth in its foundational business, Blend stands to benefit enormously from this multi-sided network that it has quietly been building.

Why it’s risky: There’s a reason that this model (lead aggregation on top of B2B infrastructure) isn’t common in fintech. Imagine if Plaid or Stripe started aggregating all the consumers that their customers drove to them and facilitating the sale of complementary products and services to those consumers for a small referral fee.

I’m guessing we’d hear some objections.

Perhaps Blend’s banking customers don’t care and never will. Perhaps there’s so much margin in mortgage that they’re comfortable with the opportunity cost of not making those referrals directly. However, if they do start to care (a possibility as Blend starts to more seriously monetize this opportunity), this bet could be in jeopardy.

A 10.9 Billion Dollar Payout

“I have always felt like I wanted to bet on myself.”

Whatever else may happen, Nima Ghamsari, co-founder and CEO of Blend, has certainly done that.

In positioning his company to simultaneously chase two different, aggressively ambitious futures, Mr. Ghamsari has demonstrated a comfort with risk taking that is unusual even for fintech founders.

And with an Elon Muskian incentive pay package of $10.9 billion on the line, he certainly has a lot to gain from those bets paying out.

Sponsored Content

Keeping up with growing information security regulations is tough, especially in fintech. With new updates and stricter laws governing data use, it’s important to know which frameworks businesses are required to be compliant with.

Laika, a hybrid software-and-services compliance platform, breaks down complex security requirements into plain-language tasks that businesses understand. They built a short, (less than 5 minutes!), quiz to help you understand which framework applies to your business. At the end, you’ll get a personalized compliance recommendation from their team of experts.

Short Takes

(Sourced from an incredible fintech news ecosystem)

What’s this then?

Lower, a home finance platform, raised a $100 million Series A. It was the company’s first external fund raise in its 7-year history.

Short take: This is quite a contrast to the prevailing trends in fintech fundraising — a fintech startup waiting seven years to raise outside capital because it was focused on achieving profitability. Pro-fit-a-bility…am I even spelling that right?

It’s about time.

MAJORITY, a mobile banking solution for migrants to the US, raised a $19 million seed round.

Short take: Digital community banks for migrants and refugees are finally becoming a thing, in the U.S. and in Europe (h/t: Nina Mohanty). Thank goodness. This isn’t a problem that would get fixed without fintech. Hopefully banks pick up some slack here as well.

I, for one, welcome our vertical-specific future.

Fifth Third Bank announced that it will acquire Provide, a platform for healthcare practices.

Short take: If the future of financial services is vertical-specific (and I think there’s a strong argument that it is), banks will need to ramp up their M&A in order to keep up. Expect more of this.

Nerd Corner

The second installment of the The Fintech Nerd Collective has been published! Our question for June was What are the most under-discussed trends in consumer fintech at the moment? There were some awesome answers, including from new nerds Jon Zanoff, Vaibhav Puranik, John Josi, and Giorgio Giuliani.

Alex Johnson is a Director of Fintech Research at Cornerstone Advisors, where he publishes commissioned research reports on fintech trends and advises both established and startup financial technology companies.

Twitter: @AlexH_Johnson

LinkedIn: Linkedin.com/in/alexhjohnson/

I’ve studiously avoided using the “selling shovels during a gold rush” analogy, but I couldn’t resist the pun there. Sorry.

TV shows are a good contrasting example. It’s generally assumed that the current wave of unbundling in the entertainment space (Netflix, Hulu, Disney+, etc.) will eventually turn into an exercise of rebundling our myriad digital streaming services into packages that look and feel a lot like cable. Read Ben Thompson for more on this topic.

How much money is Blend investing in these ecosystem partners? Consider the recently announced acquisition of Title365 from Mr. Cooper for $422 million:

Title365 will be integrated with our platform, which enables financial services firms to automate title commitments and streamline communication with consumers and settlement teams. Title365 will also expand our partner ecosystem through its network of more than 7,000 notaries.