The New Centers of Gravity in Financial Services

If the "everything is fintech" meme is where it starts, where does it end?

Programming note: I have started summarizing, on a monthly basis, the five most important trends in fintech into a short write up called 🚨Fintech Fire Alarms🚨. I’ll be publishing these in a new section of this newsletter. Subscribe here!

A popular way to think about the emergence of fintech over the last 15 years is through the lens of unbundling — startups attacking incumbents by deconstructing substandard product bundles and building better and/or cheaper individual alternatives and using those alternatives to pry away segments of incumbents’ customer bases.

Purely from a product perspective, this is a useful lens.

What it misses, however, is the deconstruction, happening in parallel, of the technical, analytical, operational, and legal infrastructure that those product bundles were built on top of.

It was this underlying infrastructure that served as a barrier for early fintech startups trying to compete with banks. Sure, you could dream up a great value proposition for underserved customers, but it was going to take you years to hammer out partnerships with sponsor banks, build the technology to process payments, and refine your fraud detection models. This time and work was prohibitive to all but the most determined fintech founders.

The emergence and maturation of fintech infrastructure companies and banking-as-a-service (BaaS) providers — which have made everything from card issuing to credit data furnishing much simpler — have significantly eroded banks’ infrastructure advantage, accelerated that rate at which customer-facing fintech companies can build, and further incentivized investors to pour money into the space.

Fintech hasn’t unbundled banking. Fintech has atomized banking.

The endgame of this atomization is to reduce every financial services function down to their most elementary version, in much the same way that Amazon ushered in the age of public cloud computing1:

Bezos became enamored with a book called Creation, by Steve Grand, the developer of a 1990s video game called Creatures that allowed players to guide and nurture a seemingly intelligent organism on their computer screens. Grand wrote that his approach to creating intelligent life was to focus on designing simple computational building blocks, called primitives, and then sit back and watch surprising behaviors emerge.

The book … helped to crystallize the debate over the problems with the company’s own infrastructure. If Amazon wanted to stimulate creativity among its developers, it shouldn’t try to guess what kind of services they might want; such guesses would be based on patterns of the past. Instead, it should be creating primitives — the building blocks of computing — and then getting out of the way. In other words, it needed to break its infrastructure down into the smallest, simplest atomic components and allow developers to freely access them with as much flexibility as possible.

If this discussion of ‘primitives’ sounds familiar it’s because the exact same approach is being taken by the latest generation of fintech infrastructure providers like Moov (emphasis mine):

Fintech infrastructure companies to date have approached the inflexible, outdated legacy banking infrastructure from the outside in. They’ve largely taken the underlying protocols as fixed, and focused instead on providing well-documented APIs and customizable UIs. In contrast to most BaaS companies, Moov is taking an inside-out approach, rebuilding the most fundamental primitives in modern Go libraries and wrapped in REST—including ACH, wires, RTP, OFAC, and a ledger for stored balance—and open sourcing them.

The availability of Moov’s primitives … will continue to fuel the creativity of entrepreneurs at companies of all sizes who will package these core primitives into original solutions.

Or, put more succinctly:

The reason that the ‘everything is fintech’ memes are funny is because they, increasingly, feel true. And the reason they feel that way is because the work of fintech infrastructure and BaaS companies has brought us to the point where literally anything can be fintech.

However, just because anything can be fintech doesn’t mean everything will be fintech. Financial services will be a better fit for certain companies and industries than others. The monetary, legal, and reputational risks won’t be for everyone. Focus will continue to be a virtue for many entrepreneurs and executives who may view financial services as a distraction from their core business.

In much the same way that the remnants of old stars, scattered by supernovas, eventually coalesce and collapse back into new stars, the atomized state of financial services will eventually coalesce around new centers of gravity.

The question is what will those centers of gravity be?

I have three guesses.

Let’s review each of these centers of gravity and parse out why they exist, how they’re evolving, and what the pros and cons are for consumers of financial services.

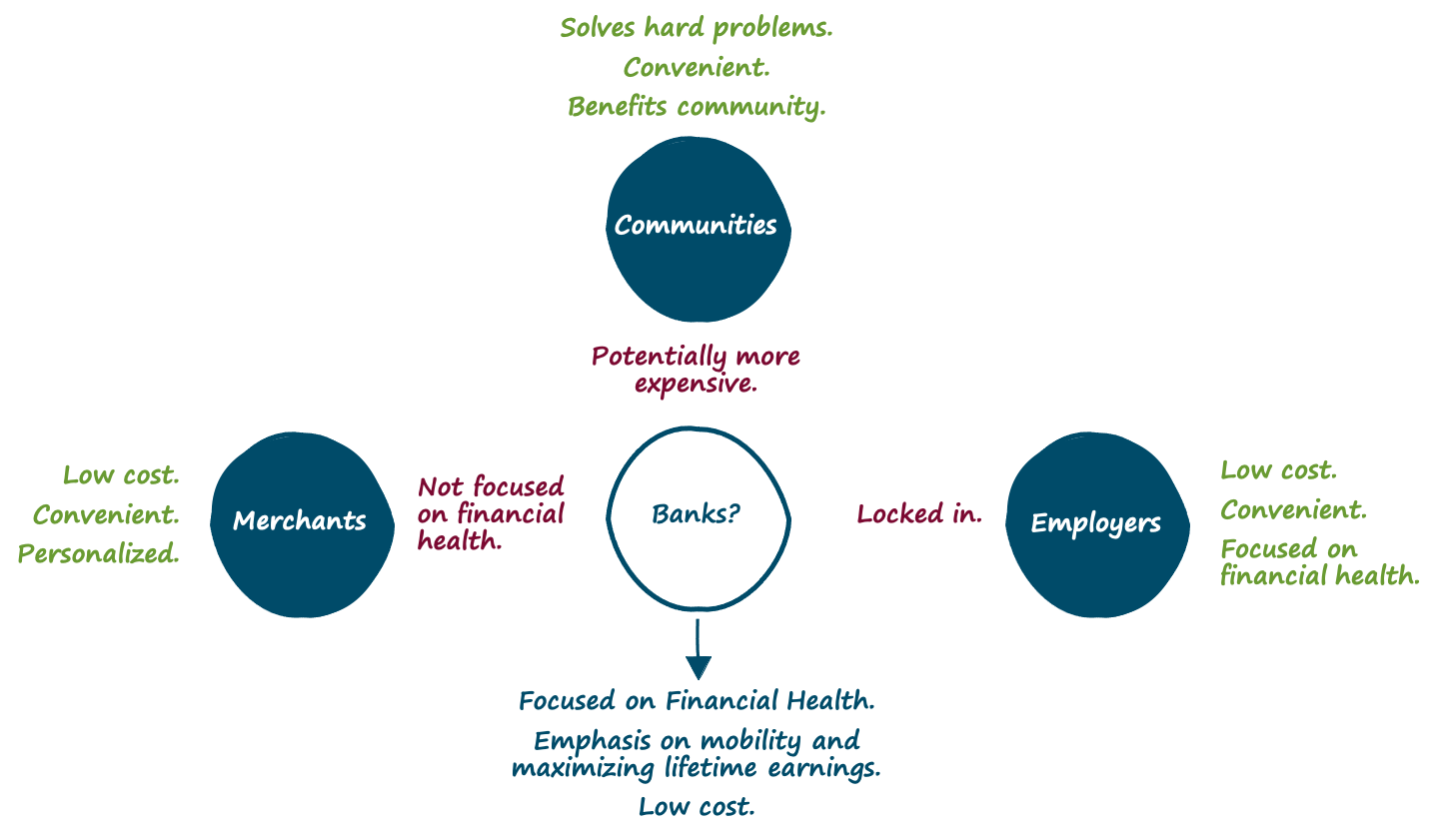

Merchants

This obviously is not a new idea. Merchants have played an important role in financial services forever. An example from the recent past is Sears, which apparently got bored in the middle of the 20th century and decided to extend its dominance in retail to insurance (Allstate), wealth management (Dean Witter), real estate (Coldwell Banker), and payments (Discover).

That might have been overkill, but it’s easy to see how certain financial products — payments, credit, insurance — are a natural fit for basically any type of merchant.

Retailers — both brick and mortar and e-commerce — want to make it as easy as possible to buy as many of their products as possible and incentivize future purchases through loyalty programs. Service providers — ranging from the big wireless carriers to the streaming services — want to bundle in as many value adds to their core services as possible in order to increase competitive differentiation and drive down attrition rates. Even the big tech platforms — your Apples and Googles — have leaned on financial services to further lock customers into their respective ecosystems.

What’s Changing?

The atomization of fintech has made it substantially easier for merchants to cost-effectively leverage financial services to strengthen their core value propositions.

Walmart provides an instructive example. Walmart has been obsessed with financial services for decades. This stems from both a strategic desire to be a a true ‘superstore’ for its customers and a deep, almost pathological dislike of the card networks. It has pursued this obsession doggedly, tackling everything from check cashing and bill payment to credit cards and Buy Now Pay Later (BNPL).

It hasn’t all been smooth sailing, to put it mildly. Indeed, Walmart has been a part of some of the most embarrassing failures in the recent history of the financial services industry; from its ill-fated attempt to procure an industrial loan company charter in 2006 to its disastrous attempt to create an alternative mobile payments system with CurrentC six years later.

What’s notable to me about these failures is just how hard Walmart had to work to even get them off the ground, in just the same way that early challenger banks like Simple and PerkStreet had to.

Compare that to the recent news that Walmart is starting a fintech company — Hazel — in partnership with Ribbit Capital and led by ex-Goldman Sachs executives Omer Ismail and David Stark and it becomes obvious just how much has changed.

No massive outcry from the banking lobby. No trouble getting access to the partners and talent necessary to bring its vision (whatever that may be) to life.

Pros and Cons for Consumers

It’s cheap (Pro). Merchants are trying to sell their core products and services. Financial services is usually an enabler of that activity rather than a primary source of revenue for these companies. This generally translates to lower prices for the end customer — 0% interest and no fees in BNPL or Google requiring that all Plex accounts come with no monthly fees, overdraft charges or minimum balance requirements.

It’s convenient (Pro). Shopping for and/or consuming a product or service is a captive experience. The merchant has the customer’s attention and control of the environment that the customer is interacting with them in. This can enable a more convenient acquisition and utilization experience for the customer. Think of Apple streamlining the Apple Card account opening experience and embedding Apple Pay natively into iOS.

It’s personalized (Pro). Merchants have a lot of data on their customers and, increasingly, how their customers are using their products. This data can be used to personalize the financial products, prices, and experiences they provide their customers, like how Tesla gives customers (in California) better insurance premiums based on their individual driving behaviors.

It’s consumption-oriented (Con). This one is obvious, but incredibly important — merchants want to provide financial products and services that drive customers to spend more money on the merchants’ primary products and services. They are not incentivized to help customers save money or make wise long-term investments. A good example is the home screens in both Affirm and Klarna’s mobile apps, which have basically become e-commerce portals.2

Employers

In the U.S., employers first started offering financial services benefits to their employees as a way to sidestep regulations signed into law by Franklin Roosevelt. During World War Two, the U.S. faced a severe labor shortage and economists feared that employer competition for talent would lead to rising salaries and, subsequently, out-of-control inflation. To prevent this, President Roosevelt signed the Stabilization Act of 1942, which froze wages and salaries and prohibited employers from competing for employees on those terms. But, as it always does, capitalism found a way around this regulatory barrier and the modern employee benefits stack (health insurance, savings for retirement, etc.) was born.

Today, employers are still investing in financial services as a mechanism for attracting and retaining employees and creating an environment in which they can be as productive as possible. PayPal’s Dan Schulman, who has invested tens of millions of dollars in his employees’ financial health over the last couple of years, is the poster CEO for the modern incarnation of this trend:

This idea that making a profit and having a purpose as a company are at odds with each other is fundamentally wrong. I actually think if you don't have a purpose as a company, you don’t see your workers as your most valuable asset and you minimize your profitability.

Research supports Schulman’s belief in a connection between employees’ financial health and productivity:

A Metlife survey of employees found that employees who were rated as “healthy” on a comprehensive wellbeing scale were “more likely to be loyal, engaged and productive, compared to those who rank poorly for all aspects of health” and that a comprehensive benefits package was a significant driver of employee well-being.

What’s Changing?

There is a whole raft of B2B fintech companies — building on top of fintech infrastructure and BaaS providers (including Payroll API companies) — focused on building “fintech as a benefit” solutions for employers, of all sizes.

A few examples:

Holistic Financial Wellness. Providers such as Brightside, HoneyBee, Origin, and Northstar focus on a providing comprehensive financial services platforms, which facilitate everything from automated savings to 1:1 financial coaching.

Employee Payments. Providers such as Branch, Even, DailyPay, and PayActiv focus on getting money into employees’ hands as quickly as possible; everything from instant tip disbursement to earned wage access.

Payroll-attached Lending. Providers like Salary Finance offer affordable loans to employees with limited access to mainstream credit by taking loan payments directly from the employees’ paychecks.

Medical Bill Negotiation. MedPut negotiates and pays unpaid medical bills on behalf of employees; drawing the payments directly from the employees’ paychecks (interest free).

Retirement Account Consolidation. Manifest automates the process of consolidating an employee’s retirement accounts from prior employers (a process that 89% of workers that switch jobs fail to do on their own).

Pros and Cons for Consumers

It’s cheap (Pro). Employers generally don’t view their employees as a direct source of revenue. These products and services are likely to be offered at cost or at a loss, which is to the employees’ benefit.

It’s convenient (Pro). Employees already interact with a variety of platforms provided by their employers, in the course of doing their jobs. Embedding additional financial products and services into these platforms creates a convenient acquisition experience. It simply becomes another checkbox in the employee onboarding process.

It’s focused on holistic financial health (Pro). If your goal, as an employer, is to keep your employees engaged and happy, then your approach to delivering financial products and services will naturally be holistic. You’ll try to reduce every aspect of financial stress (spending, saving, debt reduction, investing) in their lives.

It’s focused on lock-in (Con). Retention is the word that comes up repeatedly in this space; every provider argues that providing financial services to employees increases retention. Translation: it locks them in to working for that employer longer. This isn’t great for consumers. The ability to change jobs and even switch fields entirely is critical for maximizing a person’s earning potential over the course of their life and earning more money is the real personal finance hack.3

Communities

At the end of 2019, there were 4,750 community banks in the U.S. This is generally seen as a uniquely virtuous aspect of the U.S. financial system — a large number of small financial institutions serving the unique needs of their communities and acting as a bulwark against the big, immoral national banks. It sounds downright Capraesque.

The reality is more complicated.

Community banks have been struggling, for decades, to compete with their larger peers. Between 1990 and 2018, the number of banks in the U.S. with assets less than $500 million declined by about 70%, representing a loss of about 7,600 institutions.

This doesn’t mean that the concept of community banking isn’t valuable to customers. It just means that geography isn’t the best (or at least only) criteria for defining ‘community’.

What’s Changing?

A new generation of fintech companies are being built to better address the unique financial needs and challenges of specific communities. Because these companies rely on digital rather than branch-based distribution, the communities they serve don’t need to be constrained by geography but rather can be defined by identity. We now have banks for Black Americans and LGBT+ Americans, for new immigrants and for new parents.

Crucially, these fintech companies focus on solving critical, unsolved financial problems for their customers. Problems that traditional banks don’t even know about.

Purple, a bank for disabled Americans, is a good example. Many disabled Americans receive Supplemental Security Income (SSI) benefits. Eligibility for these benefits changes based on a person’s income; the more money a disabled person makes, the lower their SSI benefits are. This creates a perverse disincentive for disabled Americans to work and save money.

There is a potential solution — tax-advantaged savings accounts where people with disabilities can store up to $100,000 without impacting SSI eligibility and spend that money on qualified expenses.

What’s still needed, to make these savings account a functional part of a person’s financial stack, is a last-mile solution that combines a traditional checking account with this tax-advantaged savings account and automates the process of saving and spending in and out of both accounts in order to optimize the financial advantage for customers.

That’s what Purple is building.

Pros and Cons for Consumers

It’s better at solving hard problems (Pro). As the example above illustrates, these fintech companies can solve the unique problems of specific communities better than anyone. They can do this because they understand the problems better than anyone (founders in this space are almost universally members of the communities they are building for).

It’s convenient (Pro). The internet enables communities to easily self organize. This generally means that fintech companies serving specific communities have the opportunity to embed their products and services within other groups and organizations that have already formed within their communities and create a streamlined acquisition and utilization experience for their customers.

It’s mission driven (Pro). Because these fintech companies are built by the members of the same communities that they are serving, they tend to have a strong focus on steering value back to their communities. An example of this is rewards. First Boulevard — a bank for Black Americans — provides up to 15% cash back when customers make purchases at participating Black-owned businesses.

It’s potentially more expensive (Con). By focusing on a specific community, providers in this space are intentionally trading a smaller TAM for a stronger value proposition. As new, community-focused financial services providers mature, the question will be how they monetize their value propositions and how their customers react. I’m bullish, but it bears watching.

What About Banks?

The center of gravity that has held banking together for decades has been blown apart by fintech.

This has left banks with an existential question that they will spend the next couple of decades trying to answer — if a consumer can get a secure, compliant, and reliable financial product from anyone, why would they choose to get it from a bank?

It’s possible that the answer is simply “they wouldn’t”. If that’s the case, then banks will need to adapt. For smaller institutions this could mean a refresh of their community banking strategy to better compete with the Purples and First Boulevards of the world.4 For larger institutions this could mean a hard pivot to BaaS and partnerships with merchants and (increasingly) employers.5

It’s likely, though, that most banks won’t accept this answer. They will struggle to define a new, differentiated value proposition in the environment that ‘fintech atomization’ has created. A new center of gravity.

To have a chance of success, this new center of gravity needs to address the areas that merchants, employers, and community-focused providers will struggle in.

Focused on financial health. Competing on convenience is a trap. Banks can’t win there. A business model built around optimizing customers’ financial health is always going to have a competitive advantage over merchants.

Emphasis on mobility and maximizing lifetime earnings. 71% of Americans say they think about making more money a few times a week. That’s not a conversation employers want to have. Banks can and should.

Low cost. Competing on price will be critical for any bank that isn’t laser-focused on serving a specific community. Merchants and employers can afford to subsidize low prices. Banks will have to build pricing power through scale and operational efficiency.6

Sponsored Content

600+ Organizations and 1,250 industry professionals have already signed up to Fintech Meetup! They’re joining to meet 200+ Banks, Financial Services and Credit Unions, 100+ Startups, 75+ Fintech Investors and more. 34% of attendees are C-Level, and 67% are VP-Level or higher, so they’ll be talking to the right people. Don’t miss out on joining them — there’s less than 300 tickets remaining and only 19 days left to join, so Apply Now!

Short Takes

(Sourced from an incredible fintech news ecosystem)

Phishing for Coverage

Emails and websites offering payment for workplace and payroll account credentials were linked to fintech startup Argyle, according to reporting from Motherboard.

Short take: More information is obviously needed, but the implication of Motherboard’s reporting is troubling. Providers in the payroll API space are, essentially, in a race to build employee coverage. Cheating to get ahead in that race would be bad for everyone.

Bank Bitcoin Boom

FIS and NYDIG are partnering to enable a huge new swath of banks to let their customers buy bitcoin.

Short take: Consumers are rushing to buy cryptocurrencies. They are open to buying them through their banks. Banks, so far, have shown little interest in enabling this activity, but this will change (helped along by these types of partnerships).

Let’s get Dee Hock to 20,000+ Twitter Followers

Dee W Hock@deewhockDuring the five years since this site began more than 1,000 observations have been posted. While I am grateful to all who follow the site, I do not understand why it has attracted only 8,758. Perhaps someone may be able to inform me, and tell me if it is worth continuing.5:59 PM · May 9, 202130 Reposts · 733 Likes

Dee W Hock@deewhockDuring the five years since this site began more than 1,000 observations have been posted. While I am grateful to all who follow the site, I do not understand why it has attracted only 8,758. Perhaps someone may be able to inform me, and tell me if it is worth continuing.5:59 PM · May 9, 202130 Reposts · 733 LikesShort take: It’s charming and deeply relatable to see Dee Hock, the Father of Fintech, wondering why his brilliant insights haven’t earned him more followers on Twitter. Let’s get this man to 20,000!

Featured Research

Interested in learning more? Download the full report. Do you have a question that Cornerstone Advisors’ Fintech Research Practice can help you answer? I’d love to talk about it with you!

Alex Johnson is a Director of Fintech Research at Cornerstone Advisors, where he publishes commissioned research reports on fintech trends and advises both established and startup financial technology companies.

Twitter: @AlexH_Johnson

LinkedIn: Linkedin.com/in/alexhjohnson/

Source: The Everything Store by Brad Stone.

Research conducted by Capco last year revealed that more than half of 18-34 year olds using BNPL services have missed a payment and nearly two thirds say it is making them spend more, potentially increasing their chances of getting into debt.

A countervailing force is, of course, the emergence of the gig economy and the creator economy. Both of these models solve the employer lock-in issue by empowering workers to earn money independently. And both models present new financial challenges for workers, which a myriad of new fintech companies are solving for (Steady, Catch, Gig Wage, Oxygen, Thimble, Stride, Karat, Stir, Juice).

KeyBank is kinda trying to do this with its Digital Bank for Doctors.

Goldman Sachs (JetBlue, GM, Apple, Stripe) and Citi (Google Plex) are the two large U.S. banks that have shown the most interest in this strategic direction over the last couple years.

Translation: STOP BUILDING BRANCHES!