How Mid-size Banks Can Survive Fintech

Ignore the temptation of B2C, double down on B2B, and embrace verticalization.

As I’ve written before, I have a somewhat unhealthy fascination with mid-size banks.1 They have the scale and resources necessary to innovate and keep pace with big banks and fintech companies, but they’re not so flush with cash that they can survive a botched digital transformation initiative.

The strategic challenge of being a mid-size bank was the first thing I thought of when I saw this announcement:

Chime said Friday it raised $750 million in a Series G funding round that values the fintech company at $25 billion. … [the company] said it intends to invest the new capital in scaling operations, as well as launching new products and services.

As my colleague Ron Shevlin pointed out, this newest valuation places Chime right behind Fifth Third (roughly $26 billion market cap) on the list of U.S. banks with the biggest valuations.2 Reasonable people can disagree about if Chime is actually worth $25 billion, but zooming out a bit from that debate I was struck by a different thought — neobanks have now displaced mid-sized banks as the only viable competitor to big banks for consumers’ primary financial services relationships.3

I mean, Chime has approximately 20 million customers, according to recent research from Cornerstone Advisors. The company was founded 2013. Think about that. In 8 years, Chime built a digital-only customer acquisition engine that generated a portfolio that is 20 million customers strong.4

Given mid-size banks’ ongoing reliance on geographic distribution strategies (i.e. branches), I just don’t see how banks with less than $50 billion in assets will be able to compete with the retail customer acquisition engine that Chime has built (and that other neobanks are imitating and improving on).

But then another thought occurred to me — maybe they don’t need to.

For a large percentage of mid-size banks, retail banking isn’t the most important part of their business.

This feels counterintuitive. When you look at the homepage of any mid-size bank’s website, you’re likely to see a navigation menu that puts retail banking (focused on consumers) and commercial banking (focused on businesses) on relatively even footing:

However, under the surface, the majority of mid-size banks in the U.S. are heavily focused on commercial banking. And the smaller the bank, the more likely it is that commercial (both CRE and C&I) comprises a vast majority of their business (with retail representing merely a thin veneer on top).

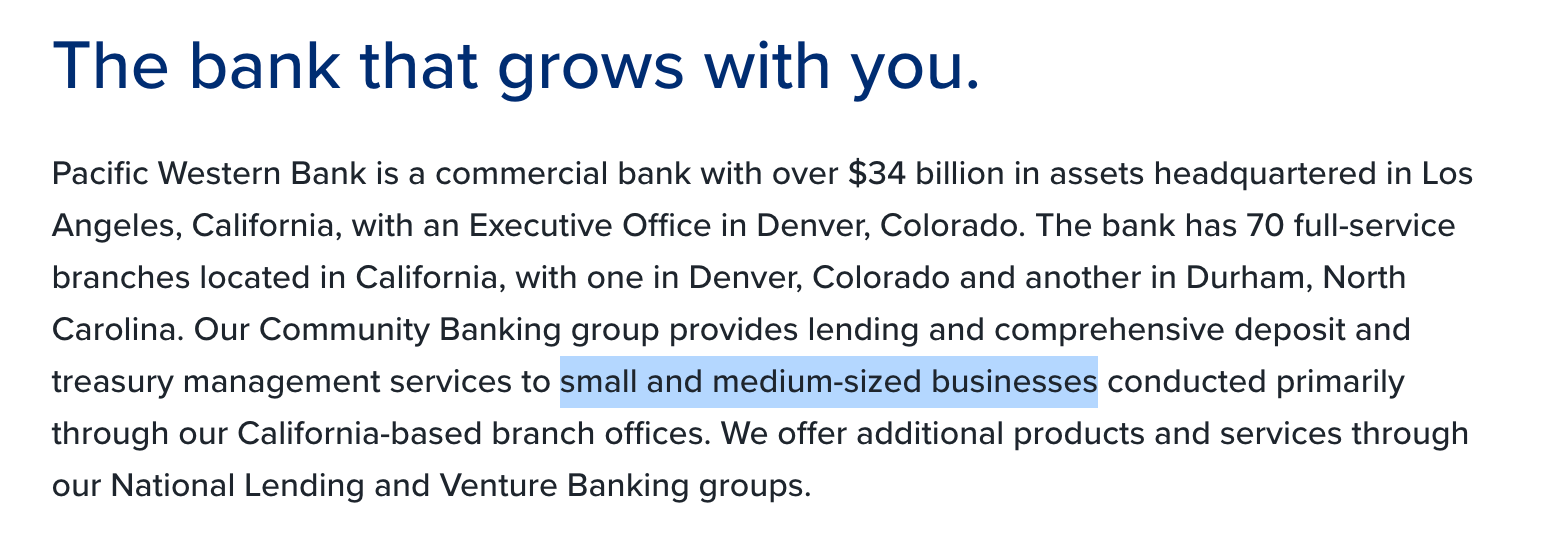

Here’s how Pacific Western Bank describe themselves on the Investor relations page on their website (emphasis mine):

For many mid-size banks, retail is, at best, a distraction from their core, money-making business. At worst, when retail banking deposits are the primary source of funding for commercial lending, it’s an unreliable crutch that’s just waiting to be callously kicked out by the big traditional banks and neobanks.

Given this, the worst thing that mid-size banks can do is let the very-well-publicized growth of B2C fintech companies tempt them into committing additional resources to fighting a losing battle in the retail banking arena.

Instead, mid-size banks should spend their time and money where they can win — in B2B banking.

Where Mid-size Banks can Win

A few things you should know about B2B Banking:

It’s massive. It doesn’t get nearly the ink that B2C gets, but B2B banking is orders of magnitude bigger. One example — according to Credit Suisse, the global market for B2B payments is $125 trillion, compared to $52 trillion for B2C payments.

It has been stuck in the dark ages. Less than 10% of non-cash payments made by U.S. consumers are made via check, compared to 50% for payments made by businesses. Fintech investment is increasingly targeting the B2B banking space, but it’s still very early.

It’s a complex and varied market. Part of the reason that the world of B2B banking has evolved as slowly as it has is because the different segments of the market (small businesses, mid-market companies, and enterprise) all have complex needs that differ tremendously.

That last point is worth double clicking into.

The B2B banking market isn’t monolithic. It’s made up of business customers that have very different needs, based on their size.

This matters for mid-size banks because some of those needs will be either difficult for them to satisfy or already well-served by existing bank and fintech service providers.

Let’s run through them real quick.

Small Businesses

Number of employees: less than 100.

Annual revenue: less than $5 million.

Market size: 31 million in the U.S. (25 million are sole proprietorships).

The average small business has 10 employees, but uses an average of 20 different software products to manage its operations. For small business owners, this is obviously less than ideal. What these entrepreneurs need is a single, comprehensive platform that can act as a ‘command center’ for managing all aspects of their business — POS, Marketing, Shipping, Inventory Management, Accounting, Payroll & Time Tracking, payments, deposits, and lending.

Small business software providers like Intuit, Square, and Shopify are extremely well positioned to deliver this type of solution and are competing fiercely with each other (and, indirectly, with banks) to do so.

Enterprise Companies

Number of employees: More than 1,000.

Annual revenue: more than $100 million.

Market size: 25,000 in the U.S.

Enterprise companies deal with an almost unimaginable level of complexity within their finance organizations, which typically span the following functions: accounting, financial planning and analysis (FP&A), capital markets, cash and liquidity management, financial risk and strategy, and supply chain financing. The goal of all of these functions, working in concert under the company’s CFO, is to maximize the return on all of the company’s financial assets.

Due to the complex and somewhat abstract nature of enterprise companies’ banking needs, large software vendors (e.g., Oracle, SAP, FIS) and corporate banks (e.g., Citigroup, JPMorgan Chase) tend to be the preferred partners for these companies’ CFOs.

Mid-market Companies

Number of employees: between 100 and 1,000.

Annual revenue: between $5 million and $100 million.

Market size: 200,000 in the U.S.

Historically, mid-market companies have not been well served by off-the-shelf banking solutions. The proverbial Goldilocks, mid-market companies are too big and complex for all-in-one small business platforms and too small to view finance as a standalone business function separated from the day-today work of running a business.

Mid-market companies rely on lean, multidisciplinary finance teams that play a strategically vital role in the overall operation of the business. Those teams need a similarly streamlined, multifunctional platform that blends all the needed banking and finance functionality with tools that can help them contribute to better strategic decisions for the business.

For mid-size banks, mid-market companies are the obvious best fit.

Mid-market companies tend to operate within similarly-sized geographic footprints to what mid-size banks operate in. Mid-market companies tend to have sticky relationships with their primary banks (average relationship tenure is 15 years). And mid-size banks just spent the last year building new relationships (and strengthening existing relationships) with businesses through the Paycheck Protection Program.

The opportunity to build better banking and finance solutions for mid-market companies is there for mid-size banks to seize, but they need to hurry because an emerging class of well-financed fintech companies are trying to get there first.

The Ideal Mid-market Business Banking Solution

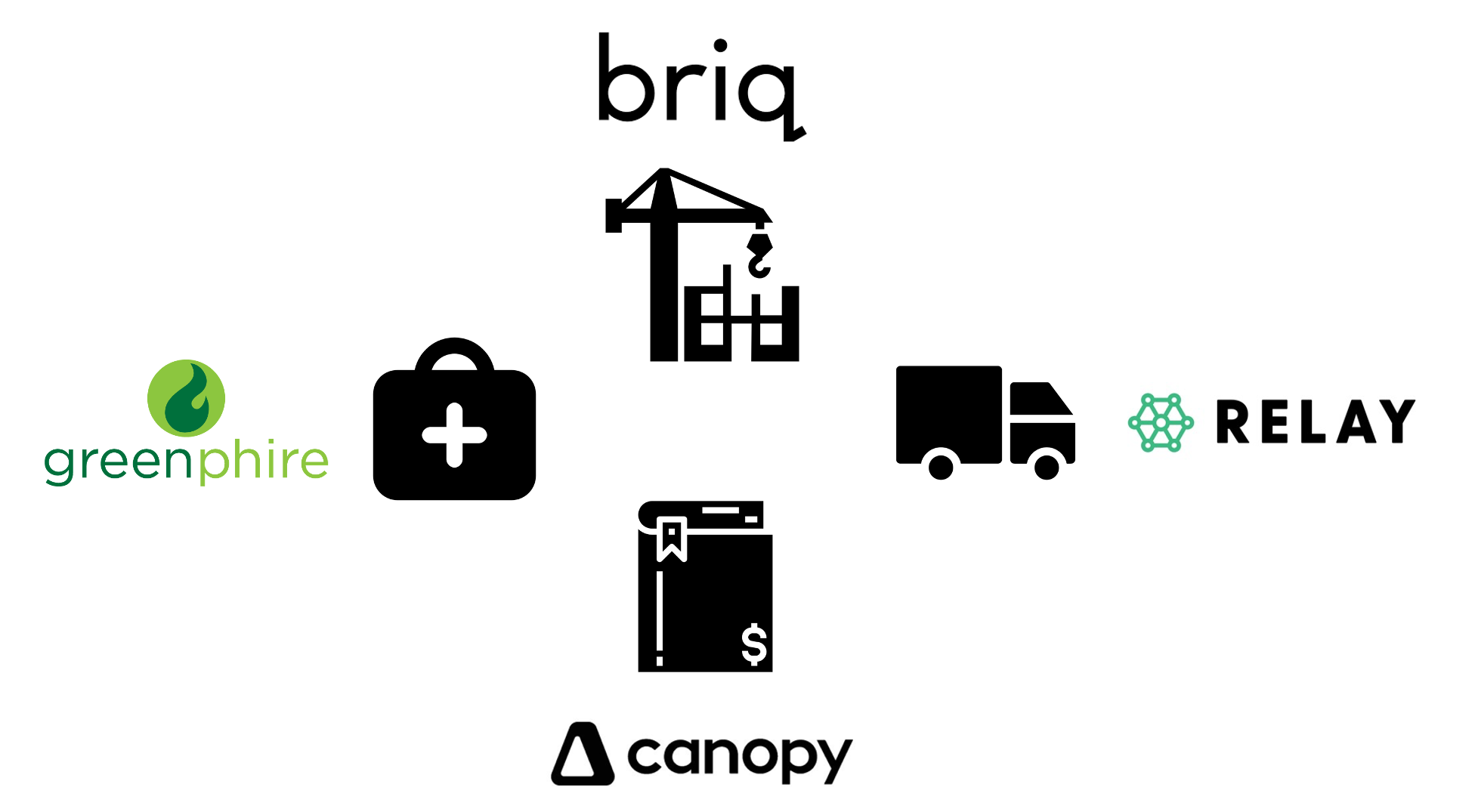

What is the ideal finance solution for the CFO of a construction company operating across six different states, with an annual revenue north of $55 million?

The founders of Briq, a B2B fintech company that just raised a $30 million Series B, would argue that the ideal solution for that CFO is a unified performance management platform that combines payments, budgeting, and forecasting capabilities with construction industry-specific data models and workflows.

How about for the project manager of a large clinical trial, sponsored by an up-and-coming biotech company?

Ask Greenphire, a provider of financial process automation software that was recently acquired by private equity firm Thoma Bravo.

What about the Comptroller at a large regional shipping company who is tired of reconciling lumper fee invoices and payments?5

Check with Relay, a B2B fintech company focused on the shipping and logistics industry that raised $43 million in Series A and B funding late last year.

Or how about the COO of a mid-market accounting firm that can no longer keep track of what each of their accountants is working on, much less the status of specific client invoices and payments?

Talk to Canopy, a provider of tax and accounting workflow management software, which just raised an $11 million Series C.

None of these companies would be likely to appear on a mid-size bank’s list of key competitors and yet, for mid-size banks that are interested in commercial clients in construction, healthcare, shipping, or accounting (read: every mid-size bank), these are the exact competitors that they should be most concerned about.

These companies aren’t banks, but they are solving the banking-adjacent problems that plague mid-market companies in these industries by smartly combining B2B banking and business management software capabilities with deep expertise in their target vertical.

If mid-size banks want to win and/or retain mid-market business customers, they need to build comparable solutions.

Next Steps

If I was the CEO of a mid-size bank with a heavy concentration of commercial customers, here’s what I would do over the next 12-24 months:

De-prioritize investments in retail banking. With increasing fintech competition in the commercial banking space, we can’t afford to waste time or resources trying to keep up with the Chimes and Robinhoods of the world. We are going to build up a base of commercial deposits, so that we can stop relying on consumer deposits to fund our commercial lending, and we aren’t going to pour anymore money into retail product development or digitization.

Pick a vertical (or maybe two). Within our commercial business, we are no longer going to try to be all things to all companies. We are going to pick 1-2 mid-market business verticals that align well with our existing commercial customer base and geographic footprint and we are going to focus all our time and resources on dominating them.

Import expertise. Within our chosen verticals we are going to double down on expertise. We are going to find executives working within our chosen industries and hire them to build the banking and finance solutions they’ve always wanted.

Become a B2B software company. We recognize that our target buyers don’t want bank products; they want software that helps them solve finance problems within the existing processes and workflows that they use to run their businesses. We will build, buy, and partner as necessary to be able to deliver verticalized business management software that combines those workflows with the necessary financial services capabilities.

Sponsored Content

Meet, network and partner at Fintech Meetup, the world’s largest fintech meetings event! Join 30,000+ meetings with 4,000 participants from 2,000+ organizations including Startups & Established Fintechs, Processors, Networks, Large Banks, Community Banks & Credit Unions, Investors and more! Discounted early bird tickets available for a limited time only, qualifying Banks and Credit Unions eligible for FREE tickets.

Short Takes

Too generic, too late.

One, a startup that aims to bring “all-in-one banking” to the middle class, announced today that it has raised $40 million in a Series B round of funding.

Short take: It feels like the window for a neobank focused on bringing a better digital banking experience to the middle class has closed. On the one hand, we have Chime and SoFi and Cash App doing that for large (and growing) segments of the market. And on the other hand, we have the traditional banks (who already have most of these middle class customers) adding fintech features like automated savings and early access to paychecks. Not sure there’s much room in the middle, unless it’s highly differentiated.

The indie version of Square + Tidal.

Nerve announced the first neobank created specifically for musicians.

Short take: This is a neat collision of fintech for small business owners (Nerve is focused on independent musicians) and fintech for creators (Nerve is also releasing Nerve FM, a direct-to-fan music streaming app).

Fintech + Barbershops

Squire, a provider of barbershop management and POS software, and Bond, an embedded finance platform, announced the launch of the Squire Card.

Short take: This is a perfect manifestation of the promise of embedded finance — a B2B software provider in a highly-specific vertical (Squire) is now able to layer fintech on top of its core offering (appointment scheduling, loyalty, etc.) through the emerging BaaS middleware layer being built by fintech infrastructure companies like Bond.

Alex Johnson is a Director of Fintech Research at Cornerstone Advisors, where he publishes commissioned research reports on fintech trends and advises both established and startup financial technology companies.

Twitter: @AlexH_Johnson

LinkedIn: Linkedin.com/in/alexhjohnson/

A rough definition of mid-size banks, for my purposes — U.S. financial institutions with between $1 billion and $50 billion in assets.

Yes, I understand that comparing a private company that investors value as a technology company against a publicly-traded company that the market values as a financial institution is like comparing apples to swordfish.

The available data backs this up. According to surveys conducted by Cornerstone Advisors, roughly one in four Gen Zers and Millennials now call a checking account from a digital bank their primary account. That’s about double the percentage it was at nine months ago.

Also yes, I know that those 20 million customers skew younger and less affluent than the average bank customer. It’s still an impressive accomplishment.

I’m guessing that sentence didn’t make a ton of sense. Short explanation: lumper fees are the fees paid by truck drivers to have their cargo unloaded at a warehouse. These fees are typically reimbursed by the shipper or broker that the driver is working with.