We're not a bank. We're a software company.

Neobanks are introducing SaaS products that we've never seen in financial services before.

If there’s one thing that unites all neobanks, it’s their insistence that they’re not actually banks. They’re software companies.

Here’s Chime’s CEO Chris Britt explaining a past valuation:

“We’re more like a consumer software company than a bank1,” Britt said. “It’s more a transaction-based, processing-based business model that is highly predicable, highly recurring and highly profitable.”

And SoFi comparing its winner-take-most opportunity to its software-as-a-service (SaaS) peers:

And Ahmed Fattouh, CEO and Chairman of InterPrivate (the SPAC that is taking Aspiration public), talking about Aspiration’s financial performance (emphasis mine):

Impressively, Aspiration can continue to grow profitability before marketing investment while maintaining strong unit economics, without taking any credit or balance sheet risk. It has software-like gross margins and strong long-term operating margins in excess of 40%. Its strong profitability is driven by high customer retention of 90% and more, and a remarkable cross sell rate with more than 1 in 2 customers signing up for a second product within the first 12 months of the relationship.

And Acorns characterizing itself as the largest subscription service in financial services:

And on and on and on. You get it. They want to be valued as SaaS companies, not banks.

That’s all well and good as a story for their investors, but the reality is that most of these companies are, in fact, banks. They provide banking products and services to consumers and they make a majority of their revenue from providing those products and services.

Sure, if you squint, they have the same general profile as software companies — digital distribution models, understaffed customer service operations, recurring subscriptions, etc. But un-squint your eyes and look at where they actually make their money and most of them are banks.

But not all of them.

A few neobanks are pioneering a new model in which consumer engagement is transmogrified into a new class of SaaS products that have never been seen in financial services before.

Building Something New

Here’s a simple truth, which we often dress up in fancy words or avoid discussing altogether — money is fun. It’s fun to earn. It’s fun to spend. It’s fun to save and watch compound. It’s fun to wager. And it’s fun to donate to good causes.

And because money is fun, financial services providers have always had an inherent advantage over companies in other industries in getting their customers to engage frequently and deeply with their products and services.

In the pre-smartphone era, this engagement was captured by traditional banks through a combination of their channels (branches, call centers, and online banking) and payment products (credit cards, most prominently).

In the post-smartphone era, banks mostly chose to see mobile as a new channel to add to their existing omnichannel strategies rather than as an opportunity to rebuild their core products in order to radically increase their rates of customer engagement.

This choice opened the door for neobanks and other B2C fintech companies to enter the market with highly differentiated mobile banking experiences, built on the principles of behavioral science and gamification.

And they succeeded in engaging their customers at a level that is, quite frankly, shocking.

Robinhood, with 47% of its customers using its app on a daily basis, is the premier example:

The question, if you are building a fintech company with this insane level of engagement, is what do you do with it? How do you monetize it? What business model do you build around it?

Do you just follow the traditional bank playbook and collect fees from your customers and try to cross-sell them your other financial products?

Nope.

You figure out how to package up that engagement and sell it as a service to someone else.

Selling Engagement

For companies running this playbook, there are three essential steps:

Build up a base of highly-engaged customers.

Leverage that engagement to build a service that you can sell to someone other than your core consumer customer base.

Scale up your new two-sided network, using growth with one set of customers to drive growth with the other.

Sounds simple, but there are a couple of challenges in spotting fintech companies that are employing this strategy.

First and most obviously, these companies look different. There are many different ways to foster a high level of customer engagement and, as a result, companies with highly engaged customer bases often appear, on the surface, to have nothing in common.

Second, a lot of fintech companies are still working on step #1. Finding new ways to monetize a highly engaged base of customers is a problem that, frankly, most neobanks would kill to have. As such, we’re still in the early innings for observing this trend in the market.

There are, however, three clear examples of companies running this playbook that I think we should talk about.

#1: Speculation-as-a-Service

The poster child for ‘Money is Fun!’ Robinhood has evolved from a low-cost alternative to traditional stock brokers into the platform for high-risk, high-return retail trading and, more broadly, meme finance.

Robinhood customers’ adventures in $GME, $AMC, and the other darlings of Reddit have been well covered in other newsletters, so I won’t delve into them here.

Suffice it to say that the last year has been good for Robinhood2 — 22.5 million user accounts with funding in them in Q2 of 2021 (a 130 percent increase from 9.8 million in the same period last year) and a market cap that has settled in, post-IPO, at roughly $37 billion.

And, as covered above, Robinhood customers engage with the app at a rate that is on par for most social media companies and utterly unheard of in financial services.

The trick, which Robinhood has mastered, is figuring out a way to package that engagement into a service that it can sell. I call it ‘Speculation-as-a-Service’, but you probably know it by a different name — Payment for Order Flow (PFOF).

PFOF is a practice in which brokers receive money for sending orders to a third-party, usually a market-maker.

When you buy $100 of Apple, for example, Robinhood (the broker) has the choice of directing your trade somewhere. While it could send your order straight to a stock exchange, market makers are usually able to offer a better price.

Instead of costing $150 per share, for example, Citadel Securities (the market maker) might be able to get it for you for $149. (The difference is usually fractions of a penny, but this is easier to keep track of.)

The result is a $1 savings. Robinhood keeps some of that, while passing on a portion to you, the user, in the form of “price improvement.” Robinhood has effectively earned money from sending your trade to Citadel Securities.

It’s worth noting that PFOF and the mechanics that sit underneath it aren’t new, unique to Robinhood, or (arguably) bad for consumers. Generally it leads to better outcomes for retail traders (price improvement), retail brokers (fee revenue), and wholesalers (a better spread on internal trades).

However, it also leads to some weird incentives.

The value of the PFOF inventory Robinhood offers is a function of two things: the number of active users and the average “noise” of their trades.

Noise is a function of both volume (number of trades) and style of trading. In general, Robinhood wants as many aggressive, high volume traders who are trading in basically random patterns as it can get.

Which helps explain Robinhood’s fondness for helping its customers not just buy stocks, but buy options on stocks.

Options — high-leverage bets on the future value of specific stocks — are profitable for Robinhood because:

(1) people may not own a ton of options, but they trade them a lot; you get more volume from options traders than you do from boring stock investors, and (2) spreads are high and it is lucrative to trade against retail options traders, so market makers are delighted to pay Robinhood large amounts of money for the privilege.

Thus, Robinhood has worked hard to become the market leader in enabling frictionless options trading on stocks and, increasingly, crypto.

Crypto comprised 51% of all transaction-based revenue [in Q2 of 2021] … more than 62% came from Dogecoin trades alone. That means Dogecoin accounted for a little more than 30% of transaction-based revenue. Against the backdrop of a decline in stock trading, it signals that Robinhood's customers are foregoing safer investments in favor of pure speculation in the crypto markets.

Money is fun. Speculation is profitable.

#2: Shopping-as-a-Service

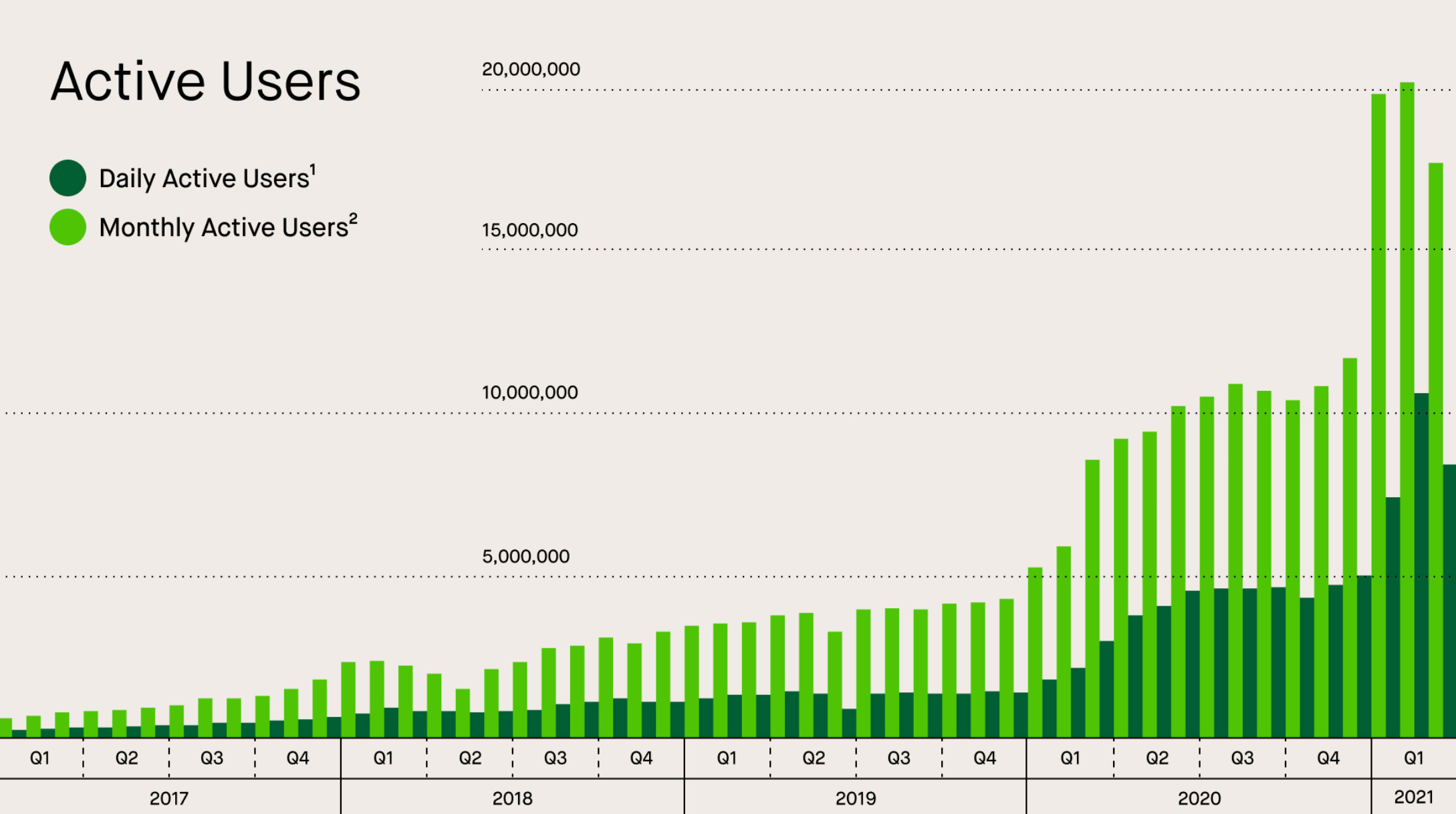

Valued at $45.6 billion, Klarna is the world’s second most valuable, privately-held fintech company (after Stripe). It is also, for better and for worse, the global standard-bearer for BNPL, with 90 million global active users across 17 countries (20 million active users in the U.S. alone).

And while Klarna’s initial wedge product was a financing tool for merchants to integrate into their websites, the company has grown far beyond that by transforming its core product into a fully-fledged shopping app.

The strategic purpose of this shift is to eliminate Klarna’s dependence on its merchant partners for customer acquisition by converting first-time Klarna customers into highly engaged shopping enthusiasts that spend increasingly large amounts of their free time in the Klarna app.

The latest numbers reported by Klarna — 18 million monthly active app users globally and 3.5 million in the US — suggest that this strategy is succeeding.

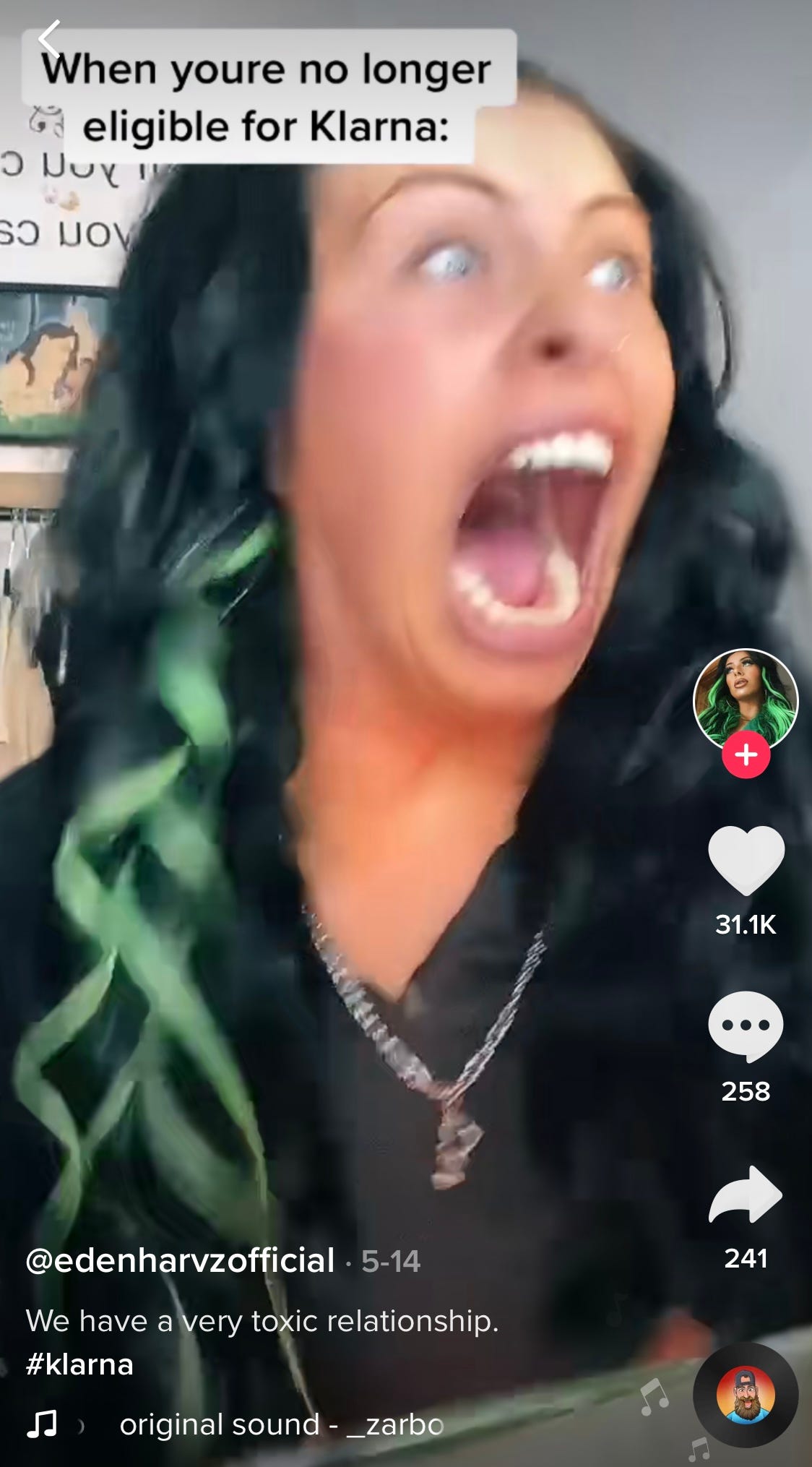

And anecdotal evidence from TikTok would suggest that describing these repeat customers as “monthly active app users” massively understates the emotional connection they feel towards the company.

It is this deeply engaged, at times unhealthy, relationship with its repeat customers that Klarna is leveraging to build out the other half of its business. I called it ‘Shopping-as-a-Service’ above, but marketers would know if by an older name — affiliate marketing.

Here’s Klarna’s U.S. leader, David Sykes, to elaborate:

A year to 18 months ago, most of our conversations with large partners were with the payments people. We were really bucketed into that payment mix, comparing us to PayPal or a traditional credit card. These days, we’re just as likely to speak to the marketing teams.

These brands are paying affiliate marketing fees of anywhere between five and 15 percent. The cost of acquiring a customer on Facebook or on Google could be anywhere between $50 and $100. So in that context, Klarna, as a source of new customers, is actually extremely competitive.We really try and drive customers to our retail partners.

For a lot of our partners, after Facebook and Google, Klarna is the number one source of net new customers. It’s a really exciting evolution of the business as the community grows.

Put simply, Klarna spent 15 years partnering with merchants to carefully cultivate a whole new generation of rabid shoppers and it is now packaging the relationships it has with that generation of customers into an acquisition service that it can sell back to those merchants.

#3: Sustainability-as-a-Service

I’ll be the first to admit — adding Aspiration, a neobank focused on serving environmentally and socially-conscious consumers, to this list feels weird. For the record, I love Aspiration’s mission and if its somewhat complicated business model (explained below) helps catalyze progress towards mitigating the impacts of climate change, I’ll be thrilled.

That said, if you look under the hood, Aspiration is strikingly similar to Robinhood:

Both offer banking and investing services with no fees3 and premium versions of those services for a fee.

Both offer deposit products as licensed broker-dealers (regulated by the SEC), which means that they sweep cash deposited by customers into a network of FDIC-insured partner banks.4

And both have transformed the large, highly-engaged customer bases that they have built into new services that they can sell. For Robinhood, that’s PFOF. For Aspiration, it’s Sustainability-as-a-Service.

The most surprising thing in the investor presentation that Aspiration put together for its upcoming debut on the public markets was the fact that a majority of the company’s revenue doesn’t come directly from its 5 million consumer customers.

What exactly are corporate ESG impact services, you ask?

As best I can tell, Aspiration has leveraged demand from its consumer customers in order to negotiate favorable deals for carbon offsets — they claim to have a 20-year locked price on more than 5 billion trees — in order to offer that inventory of offsets to corporations (which have a rapidly growing appetite for ESG investments) at a highly competitive price.

Something Different

Leveraging consumer customer engagement in order to create and sell new SaaS products to corporate customers isn’t necessarily a bad thing. Nor is it necessarily good. It is, however, undeniably different.

And different can be challenging if it confuses consumers (“Buy now, pay later is being dressed up as a glamorous payment option … Its true nature as a credit or debt product was really pretty difficult to actually decipher.”) or doesn’t fit neatly into established regulatory frameworks (“They get the data, they get the first look, they get to match off buyers and sellers out of that order flow … That may not be the most efficient markets for the 2020s.”).

Sponsored Content

Fintechs have helped millions of people increase their financial well-being, but for many of these users, insurance continues to be a financial stressor. Users are increasingly turning to the financial services they trust for a solution that solves their insurance needs.

Savvy is the leading solution in the market that enables fintechs to build a white labeled, embedded insurance offering. Savvy helps fintechs build best-in-class insurance experiences that bring real value to their users. Turn insurance into a monetization engine that delivers users meaningful savings through a highly differentiated, native experience.

Connect with Savvy about a custom solution by following the link below!

Short Takes

Get ready for massive B2B fintech valuations.

Melio, a payments startup, is raising funds at a $4 billion valuation.

Short take: Just a couple of years ago this company was automating AP for wine shops in NYC. Today they are raising at a $4 billion valuation. I guess that’s what a partnership with Capital One, a write up in Not Boring, and attacking a $10 trillion market with a strong product gets you.

Building the infrastructure for BNPL.

Ikea bought a minority stake in buy-now-pay-later provider Jifiti for $22.5 million.

Short take: Jifiti is part of a growing class of fintech infrastructure providers, along with Amount and a few others, focused on helping banks and merchants build white label BNPL solutions. Expect a lot more activity in this space.

An 800-pound gorilla stomps into the ID scanning market.

Apple is adding drivers’ licenses to its digital wallets.

Short take: Assuming Apple keeps adding States and Google gets into the game (both likely, IMO), this will mark a huge shift in the KYC vendor ecosystem. For more, I highly recommend Jason Mikula’s recent newsletter.

Nerd Corner

A new month means a new question for the Fintech Nerd Collective — What at the moment looks like a toy in fintech, but will end up being the next big thing?

Answers included influencer marketing, QR codes, neobanks for digital-native communities, tools for democratizing shareholder influence (mine), and, of course, NFTs.

Alex Johnson is a Director of Fintech Research at Cornerstone Advisors, where he publishes commissioned research reports on fintech trends and advises both established and startup financial technology companies.

Twitter: @AlexH_Johnson

LinkedIn: Linkedin.com/in/alexhjohnson/

The irony of Chime describing itself to investors as a software company and getting dinged by the California Department of Financial Protection and Innovation for not making it clear enough to customers that it’s not a bank is quite something.

With, admittedly, some bad — service interruptions, Congressional hearings, record-breaking fines — mixed in.

Aspiration does ask customers to sign up for a monthly account fee at whatever price they “think is fair”, which I find utterly infuriating. See this thread for details:

This sweep arrangement can, in the worst case scenario, cause additional problems for customers because their money is stored in bank accounts that they can’t directly access. See the story of Beam Financial for the gory details.