A Tale of Two SPACs

Building a successful neobank is hard. Recent SPACs illustrate why.

Editor’s note — this newsletter is the result of a collaboration with Ryan Martin, an expert on all things fintech with an excellent eye for malarkey hiding in investor presentations.

When it was reported that Google was canceling its Plex checking account product, a common response from folks working in fintech looked like this:

And while I might feel inclined to search for more complex answers to the question of why Google (and many who have come before it) have failed when trying to launch banking products, the simplest answer is usually the best.

Building a neobank1 is hard!

It’s hard, I think, for two reasons:

You have to build a functioning bank, with solid unit economics and a reliable and efficient operating model.

You have to develop and deliver on a disruptive brand promise that meaningfully differentiates you from the legacy financial institutions you are trying to displace.

Now, of course, it’s basically impossible for fintech companies to do both of these things well when they’re first getting started.2 Typically fintech companies will focus a majority of their resources on #2 and will adopt a lean, fake-it-till-you-make-it approach to #1.

And that’s OK! Neobanks don’t need to own their own charter or have a fully-staffed customer service call center up and running on day one. They don’t even necessarily need to have the unit economics part fleshed out immediately. The current VC ecosystem is patient and well funded. They will provide aspiring neobanks that they believe in with a lot of runway.

However, eventually every neobank needs to figure out how to run a profitable bank and deliver on a disruptive brand promise at the same time.

Chime is a good example.

Chime is the largest and most successful neobank in the U.S. because it made a simple, compelling brand promise — to create better, lower-cost options for everyday Americans who aren’t being served well by traditional banks — and it slowly and methodically built a competent, well-run business around that brand promise. The company’s most compelling features — fee-free overdrafts, early access to direct deposits, credit building — aren’t radically new ideas.3 They’re just thoughtful tweaks on existing bank products and business models, all aligned with Chime’s brand promise to better serve everyday Americans.

It’s kinda boring, but that’s exactly the point. There’s a reason you don’t see Chime leaping to enable the buying and selling of Dogecoin or introducing BNPL just because everyone else is. Chime’s defining characteristic is discipline.

And judging by its latest investment round, which valued the company at $25 billion, it’s clear that this discipline is being rewarded by late-stage private investors.

The interesting part, to me, is seeing what happens to the other neobanks chasing after Chime; the ones that maybe don’t have the same discipline to both build a strong business and deliver on a disruptive brand promise. What happens when their runway runs out? How will late-stage private investors and the public markets treat them? How far will the sheen of being a fintech company carry them when the underlying fundamentals don’t tell a great story?

To start answering these questions, we need to find an easy way to identify and analyze mature neobanks that may be struggling with these challenges. Some mechanism that simultaneously indicates corporate distress and provides insights into the nature of that distress.

I’ve got it! What about SPACs?

This line from a recent edition of Nik Milanović’s excellent newsletter caught my eye:

Early investors are dumping SPAC deals once they go public, leaving day traders to rush in … this isn’t surprising: SPACs are generally the only path to liquidity for distressed tech companies.

Perfect!

A Tale of Two SPACs

There are two neobanks — one that recently went public via a SPAC and one that is on its way — that illustrate the challenges inherent in both building a good bank and executing on a disruptive brand promise.

I will provide an overview of each company and point out a few of the more glaring oddities from their investor presentations and what I think they mean.

Aspiration — Is this sustainable?

SPAC Valuation: $2.3 billion

Overview: Aspiration is a neobank focused on serving climate-conscious consumers that want the financial services products that they use to positively benefit the environment and society. Aspiration attempts to deliver on this promise by offering standard financial products — checking and savings, debit card, credit card, investing — with differentiated features designed to help customers fight climate change. For example, Aspiration’s newly launched credit card rewards customers by planting one tree every time they use their card and helps customers track their carbon emissions and offsets. In addition to its consumer-facing business, Aspiration also provides carbon offsetting services to other companies, leveraging the deals it has already made with reforestation partners in order to offer extremely competitive pricing.

Challenge: By virtue of its very laudable mission, Aspiration is certainly executing on a compelling brand promise. However, from the information made available via its SPAC merger, it’s not clear if Aspiration has figured out how to run a profitable banking business yet.

A few observations:

Aspiration claims to have a “Strong Brand and Community of over 5 million passionate, purpose-driven members”.

However, in the fine print they define members as “the cumulative number of members who have signed terms and conditions to open a brokerage cash management account with Aspiration Finance LLC or an investment management account with Aspiration Fund adviser LLC (whether or not they are still registered for such products) in a given product.” The actual number of funded accounts, at the end of 2020, was 360,835.

I’m all for a little creative counting, but having 7% of the total number of customers you claim to have is an unusually big fib.

You’ve heard of EBITDA — Earnings Before Interest, Tax, Depreciation, Amortization. Pretty standard. How about EBITDAM? The ‘M’ at the end stands for marketing and it’s an addition you make to the acronym when you really need to not count marketing expenses in your profitability calculations.

Aspiration spent $22 million on marketing in 2020. In 2021, it estimates that it will spend $149 million.4 By 2023, Aspiration estimates that it will spend $332 million on marketing.

Putting all of this in context, Aspiration made $14.7 million in total revenue in 2020.

Just over 30% of that revenue came from Aspiration’s financial services products. 69% of revenue came from “ESG services”, with “corporate ESG services” taking up a lion’s share (56% of total revenue).

As mentioned above, “corporate ESG services” is basically selling carbon offsets (via reforestation5) to other companies, drawing on the inventory of carbon offsets that Aspiration has already acquired for its consumer customers.

Can Aspiration ramp up its consumer banking revenue in order to balance out this mix and become less reliant on corporate ESG services (a space that seems guaranteed to become more competitive in the next decade)?

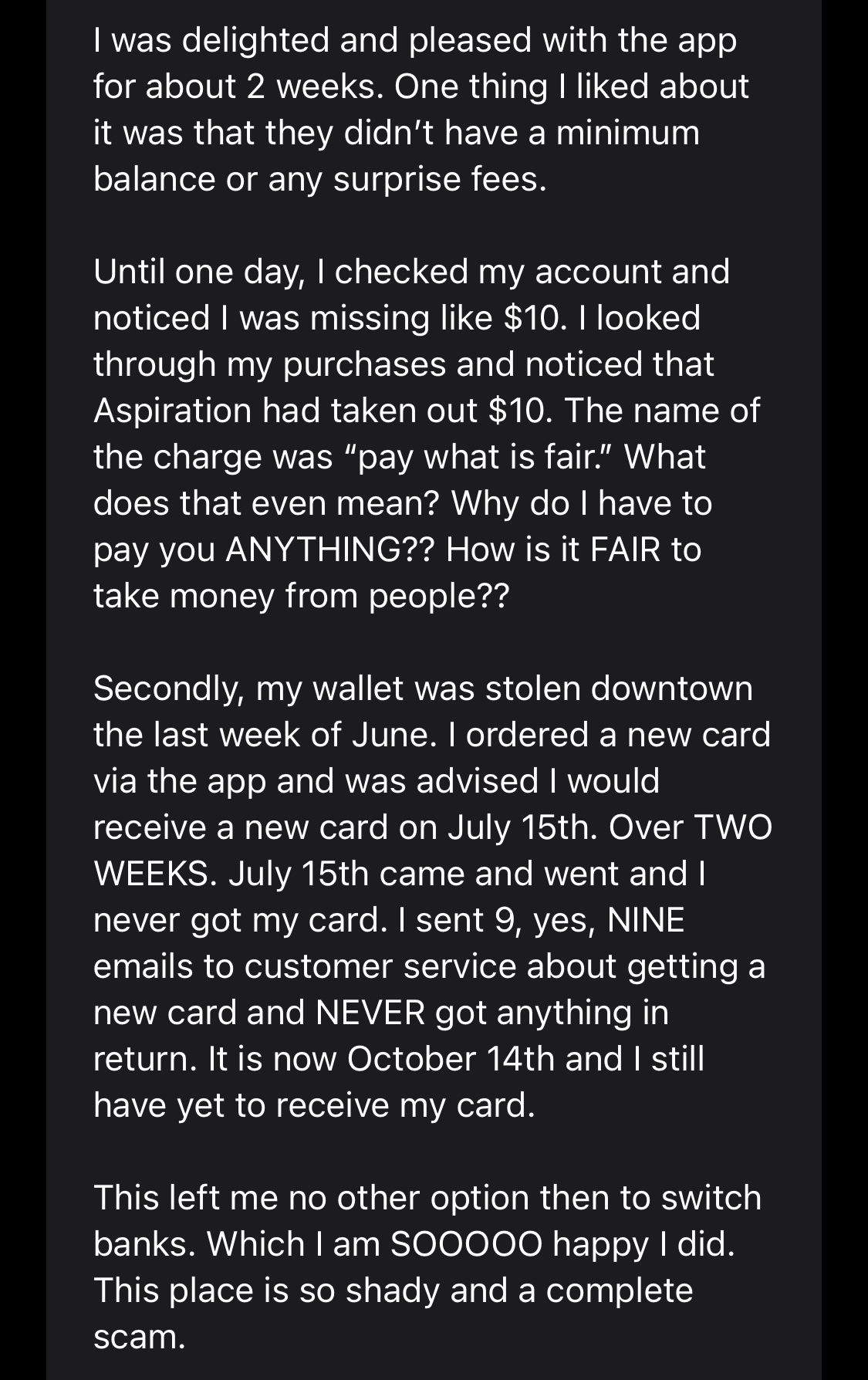

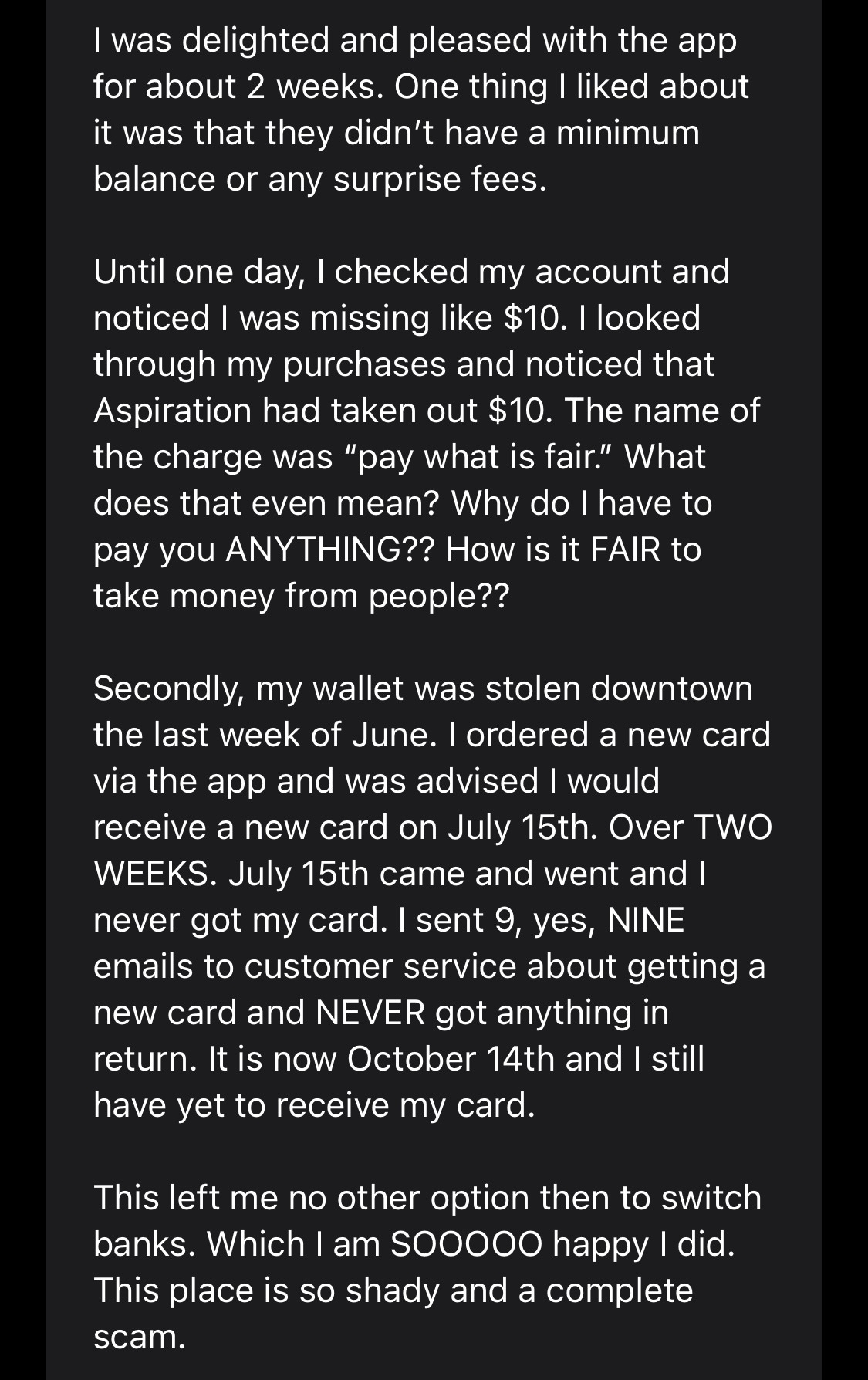

It certainly seems to think so. It projects that it will grow from roughly $30 million in non-ESG consumer revenue today to $725 million in 2024, a 24x increase. This seems extremely optimistic, particularly when you consider that customers seem to have mixed feelings about Aspiration (judging by App Store and Better Business Bureau reviews). Here’s one recent example, from the iOS App Store:

The “pay what is fair” fee referenced in the customer review above is, unbelievably, a real thing. It’s an example of a uniquely terrible trend in fintech — dressing up the costs of providing banking services in ‘voluntary fees’ and ‘tips’ rather than just being honest with customers. For a longer rant on this subject, check out this Twitter thread:

Alex Johnson@AlexH_JohnsonNeobanks are getting too cute with their fees and revenue models. Enough with the voluntary tips and the only-pay-what-you-think-is-fair account fees. Your customers are adults. They understand stuff costs money. Just be honest with them. 🧵

Alex Johnson@AlexH_JohnsonNeobanks are getting too cute with their fees and revenue models. Enough with the voluntary tips and the only-pay-what-you-think-is-fair account fees. Your customers are adults. They understand stuff costs money. Just be honest with them. 🧵 2:55 PM · Aug 25, 20215 Reposts · 33 Likes

2:55 PM · Aug 25, 20215 Reposts · 33 LikesCharge a fee or don’t. Charging an optional fee that both pisses off customers and doesn’t deliver a reliable revenue stream is just bad business.

TL;DR: Aspiration has built a machine that turns consumer marketing spend into carbon offset inventory for B2B ESG sales. Given the intensifying competition in ESG and the rising costs to acquire financial services customers, this doesn’t seem like a machine that one would want to own long term. We’ll see if Aspiration can leverage its planned burst of marketing spend to transform that machine into something that looks and performs more like a bank.

MoneyLion — All roar, no bite.

SPAC Valuation: $2.4 billion

Overview: MoneyLion is a neobank that is focused on the 100+ million consumers in America’s middle class, who are, in MoneyLion’s words, “disadvantaged by the current financial system.” It attempts to do this by offering a broad array of financial products — checking account, cash advance, credit builder loan, BNPL, investment account, crypto — and an overarching financial advice platform that helps guide customers’ financial decisions and recommends new products (MoneyLion’s and third parties’).

Challenge: MoneyLion ships a lot (crypto and BNPL are the newest products to be introduced this year) and it has built a number of different revenue streams off of its more than 2 million customers. It has the ‘bank’ part of being a neobank down pretty well. However, a close look at the company’s products and business model suggests that its brand promise to help “hardworking Americans” by “rewiring the banking system” might not be one that it is keeping.

A few observations:

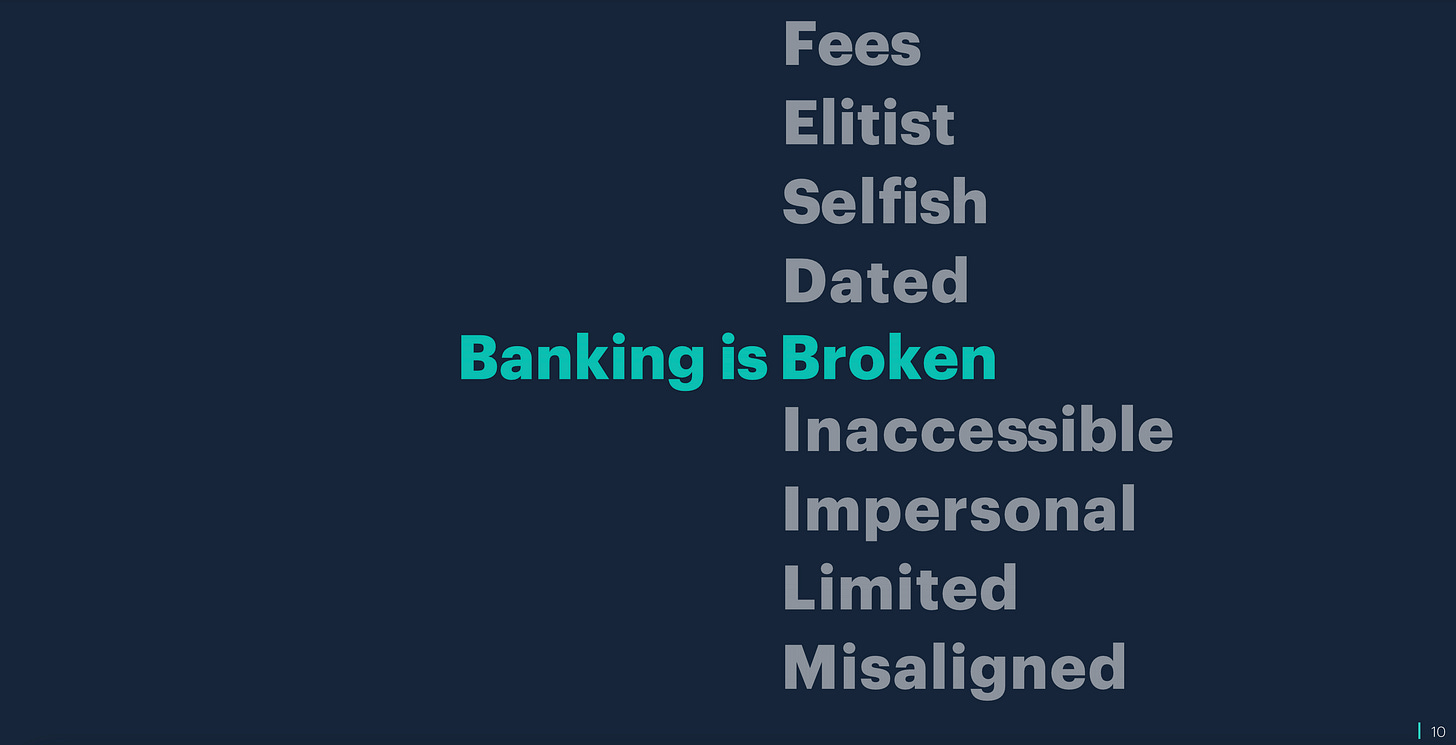

This is my favorite slide from MoneyLion’s first Investor Presentation from back in February, 20216:

Standard fare in the fintech world, but it rings a bit false here. First of all, the claim that banking is elitist is a bit rich coming from a company whose co-founder and CEO is a former investment banker, with stops at Barclays, Citadel Securities, and Goldman Sachs.

MoneyLion also claims that banking is broken because of banks’ over reliance on fee income. This is fascinating given that 81% of the revenue that the company was earning at the end of 2020 was from fees.

That ratio has changed a bit in 2021 — the percentage of revenue from fees was down to 77% by Q2 of 2021 and payments was up to 10% — and is expected by the company to shift even more towards payments and advice by 2023. The catch, however, is what MoneyLion considers “payments” and “advice” revenue.

Ohh, hey! More fees!

Instacash, MoneyLion’s cash advance product, is a ‘free’ product that presents a truly impressive number of opportunities to pay for it.

The company says that it “designed Instacash to help you access smaller amounts of cash in a pinch, such as for an unexpected late fee, a can't-miss date night, or to avoid a costly overdraft charge.” These use cases suggest that MoneyLion customers utilize this feature when they need money immediately, but the problem (for the customer) is that they have to pay a “Turbo fee” of $3.99 or $4.99 in order to get the funds quickly.

During each Instacash transaction MoneyLion also requests that the customer pay an optional tip. The tip is optional, but I’m guessing that the default tip amount suggested by the MoneyLion app isn’t $0. The company has the gall to remind customers, when explaining these optional tips, that “we’re all in this together!”.

And one final, fun twist — even though the maximum amount of money available for customers to advance can get as high as $1,000, they can only take it out in increments up to $50, which has the obvious upside of giving MoneyLion more bites at the apple to earn fees and tips.

MoneyLion’s credit builder loan is even more remarkable.

Customers borrow up to $1,000, at an APR between 5.99% and 29.99%. In addition to the interest rate, customers pay a $19.99 monthly fee for the product. So, For a 12 month loan of $1,000 at 5.99% APR, customers would pay a total of $267.17 in interest and fees. At 29.99% APR, customers would pay $409.67.

And, of course, it’s a secured credit builder loan, so the customer doesn’t actually get the $1,000 up front. They get a small portion of it and the rest is set aside in a Credit Reserve Account that MoneyLion holds in case of default (and earns interest on in the meantime).

Customers can offset the $19.99 fee (or a portion of it) by meeting certain, totally reasonable engagement thresholds:

TL;DR: MoneyLion does a masterful job of using fintech framing (banking is broken) to burnish its brand and tee up its brand promise (rewiring the banking system for hardworking Americans), but there’s a big difference between making a promise and delivering on it. With its current products and business model, MoneyLion has quite a ways to go to close that gap.

The end of the runway.

It’s never been easier to build a bank. The blueprint, the infrastructure, the financing, the talent; all of it is readily available.

This ease has, perhaps, obscured another truth — it’s incredibly difficult to build a successful bank. It’s difficult in ways that BaaS platforms and deep-pocketed VC firms can’t fix.

MoneyLion is learning this lesson right now. Having successfully merged with Fusion Acquisition Corp to become a public company (NYSE: ML), MoneyLion is currently valued at a little more than $1.3 billion, which is roughly half of what it was valued at when the merger was first announced back in February.

At a time when fintech has never been hotter — $4.5 billion in equity raised last week — this is actually comforting. At the end of the day, a neobank will only be as successful as the public markets judge its business to be and as its customers judge it to be at keeping its brand promise.

Sponsored Content

Fintechs have helped millions of people increase their financial well-being, but for many of these users, insurance continues to be a financial stressor. Users are increasingly turning to the financial services they trust for a solution that solves their insurance needs.

Savvy is the leading solution in the market that enables fintechs to build a white labeled, embedded insurance offering. Savvy helps fintechs build best-in-class insurance experiences that bring real value to their users. Turn insurance into a monetization engine that delivers users meaningful savings through a highly differentiated, native experience.

Connect with Savvy about a custom solution by following the link below!

Short Takes

Too big to fail?

Fintech startup N26 has raised a $900 million Series E round at a $9 billion valuation.

Short Take: The $900 million will reportedly be used to help N26 pull back from its international ambitions and focus on Europe and its core products … which seem like strategies that would save money not require more money? Serious question — is it possible for fintech companies to strategically languish and yet be too big to fail?

The untapped NFT market.

Coinbase is working on an NFT marketplace.

Short take: OpenSea owns 97% of the NFT market, which suggests to me that Coinbase believes there is a substantial population of new consumers who would buy NFTs if they were easier to browse, purchase, and sell. I’m fascinated to see how this bet plays out.

The OG DAO.

Beneficial State Bank became the first American bank to unionize in 40 years.

Short take: For the kids out there who may be unfamiliar, a union is a collection of employees that band together to exert greater control over their jobs and protect their common interests.

Alex Johnson is a Director of Fintech Research at Cornerstone Advisors, where he publishes commissioned research reports on fintech trends and advises both established and startup financial technology companies.

Twitter: @AlexH_Johnson

LinkedIn: Linkedin.com/in/alexhjohnson/

Google wasn’t, precisely, trying to build a neobank with Plex, but it was certainly neobank-y.

It’s harder today than it was 10 years ago. Building a strong banking business is much more difficult with skyrocketing customer acquisition costs and delivering on a distinct brand promise is much more difficult when you’re surrounded by me-too neobanks and aspiring fintech brands.

They were somewhat radical ideas at the time Chime launched them. It’s important to put Chime’s success in the context of the first mover advantage that it seized. Chime’s core features are table stakes for neobanks today.

One big marketing line item for 2021? A $300+ million sponsorship of the LA Clippers’s new arena. A bank with 300,000+ funded accounts spending $300+ million on a brand sponsorship is certainly something.

It’s worth noting that reforestation — planting trees to offset carbon emissions — is a controversial intervention among scientists.

Minor mystery — the first investor presentation from February was replaced by an updated presentation in September and the February version was removed from MoneyLion’s website.