Leveling The Playing Field

Banks' lobbying efforts and current digital transformation initiatives won't save them.

You may have noticed a certain amount of complaining to the refs happening in financial services lately.

Here’s Jamie Dimon on unfair competition from fintech companies:

People who we will make a lot more on debit, because they activate under certain things, the only reason they compete is because of that. People you know, basically, don't do KYC AML and create risk for the system. And I can go on and on, but that part we will be a little bit more aggressive on, people who improperly use data has been given to them by client, OK? So you can expect that there will be other battle to take place here.

And Richard Hunt, President and CEO of the Consumer Bankers Association, on fintech companies gaming the Durbin Amendment:

Large fintechs are exploiting loopholes created by a bifurcated regulatory system. As a result, these large fintechs with tens of billions in assets are playing by rules created for small community banks.

And Ana Botín, executive chairman of Santander, on the need for a regulatory reset in banking:

Regulation now favours tech companies that intermediate financial services over banks. This is especially true for the rules on data, which powers payments.1 Large tech companies are becoming lending platforms without having to comply with most banking regulation. Their role, although still relatively small overall, is growing. Last year, fintech and Big Tech credit reached $795bn globally, according to the Bank for International Settlements. The pandemic will only entrench the digital players. We need to level the playing field — not to give banks an advantage, but to remove the advantage that tech companies have had for the last 10 years.

That statement from Ana Botín perfectly summarizes the foundational desire that banks have when it comes to competing with fintech companies — a level playing field.2

That same desire is warping many banks’ strategic priorities.

An Easy Explanation and Effective Excuse

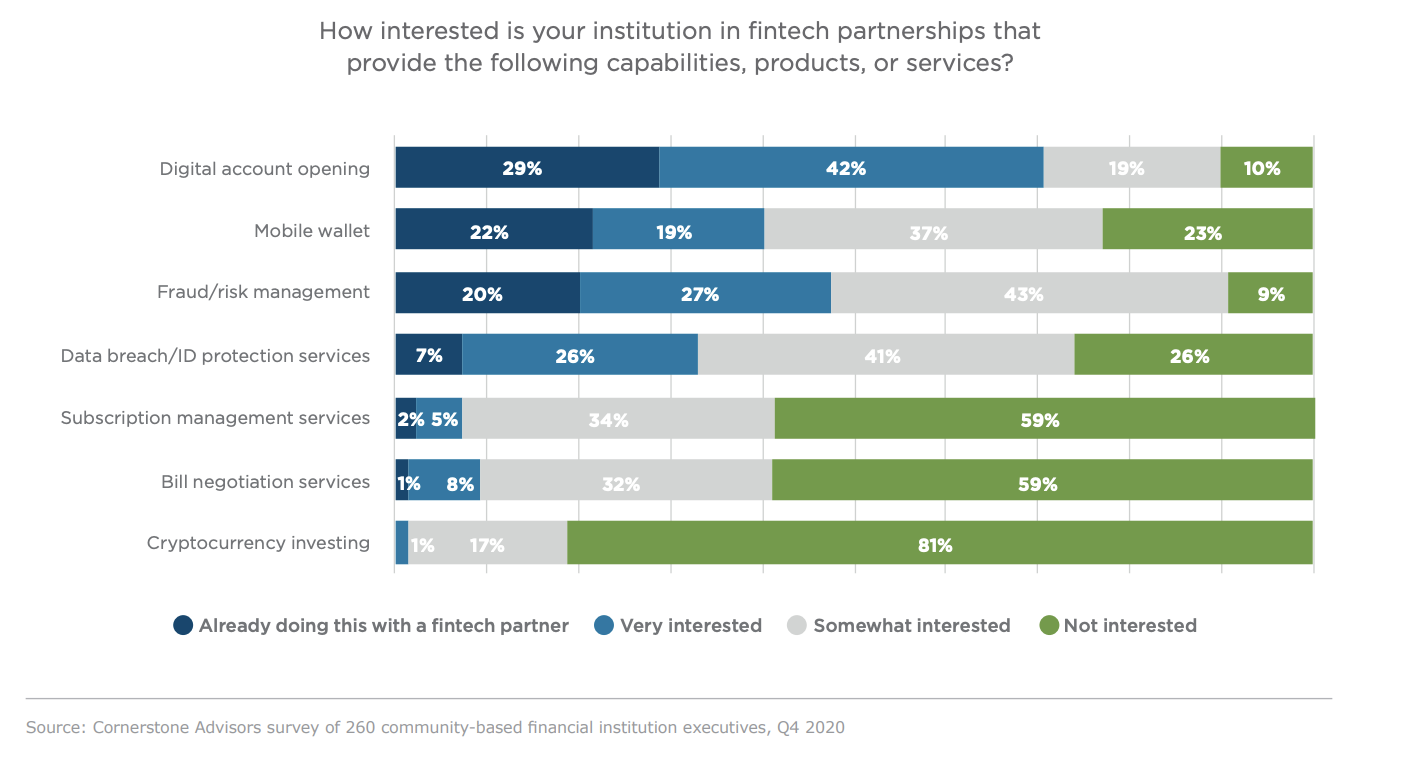

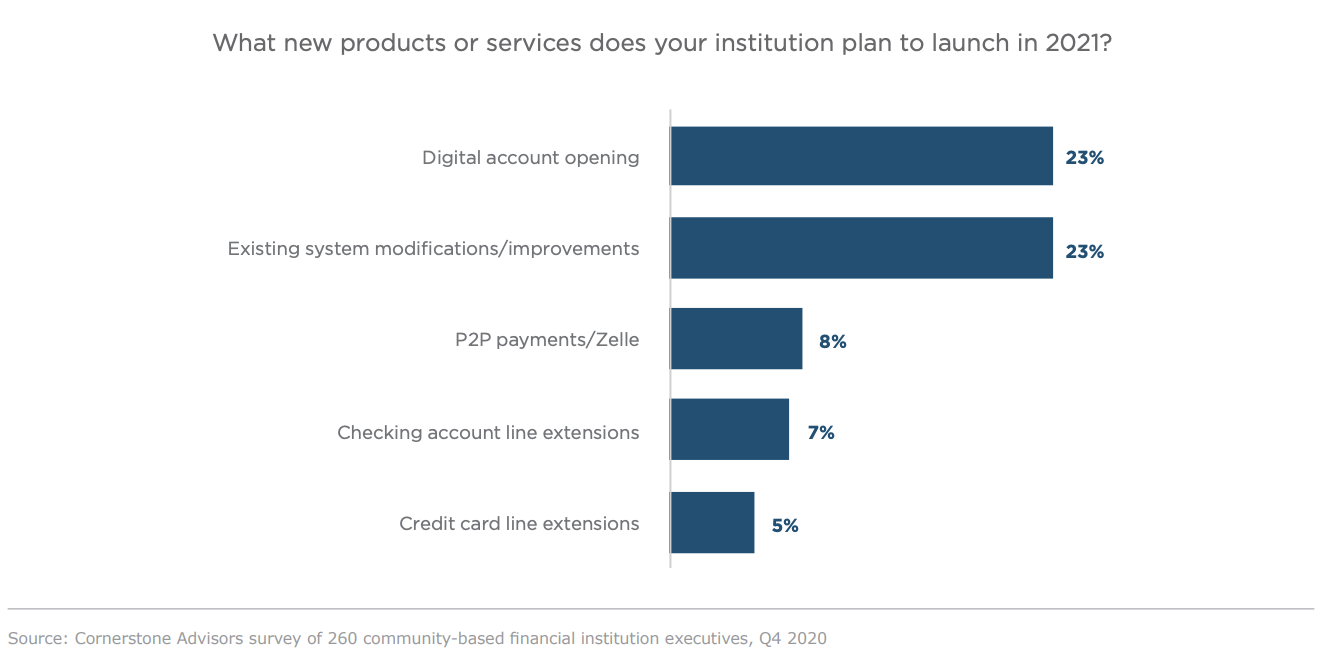

In Cornerstone Advisors’ What’s Going on in Banking 2021 report, we asked mid-sized U.S. banks what technologies they were planning to buy or replace in 2021, the most popular answer was, for the fourth consecutive year, digital account opening.

We asked what their priorities were for fintech partnerships in 2021 and, again, digital account opening was #1.

We also asked what new products or services they are planning to launch in 2021 and the most popular response was, you guessed it, digital account opening!

I think banks are obsessed with digital account opening because it’s an easy explanation for fintech companies’ success and an effective excuse for not making bigger, more difficult changes inside their own companies.

I mean look at that last question —what new products and services does your institution plan to launch in 2021? Digital account opening? That’s not even a bank product! That doesn’t make any sense!

The only logical way to interpret that result is to start from the assumption that mid-size banks think their actual products (deposit accounts, loans, etc.) are just fine the way they are and that all they need to do to win in the market is get that fancy digital account opening thing that fintech companies have.

In other words, banks just need to level the digital playing field and then they’ll be able to compete and win against fintech companies.

The problem with this line of thinking is that the hallmarks of digital transformation — digital account opening, APIs, machine learning — aren’t the source of fintech companies’ innovation, they’re simply the byproducts of a deeper culture of innovation.

When Copying Fails

A similar dynamic has been playing out in the social media space.

The story of social media during the last decade was one of Facebook’s dominance. The largest social network in the world was also the most ruthlessly competitive, blatantly copying the features of any upstart that dared challenge them. Here’s Casey Newton on the (supposed) death of competition in social media:

If I had to put a date on when competition ended among social networks in the United States, I’d choose Aug. 2, 2016. That’s when Instagram introduced its copy of Snapchat stories, blunting the momentum of an upstart challenger and sending a chill through the startup ecosystem. … the effect of Facebook’s copying here was dramatic. Snap fell into a long funk, and would-be entrepreneurs and investors got the message: Facebook will seek to acquire or copy any upstart social product, dramatically limiting its odds of breakout success. Investment shrunk accordingly.

It got so bad that Kara Swisher started half-jokingly referring to Snap CEO Evan Spiegel as Facebook’s Chief Product Officer.

Then something strange happened — disruptive innovation in social media exploded.

TikTok is the obvious example.

The success of TikTok is a source of real anxiety inside Facebook, where employees ask CEO Mark Zuckerberg a question about it during nearly every all-hands Q&A session.

But there’s also Clubhouse.

Facebook has been sufficiently intrigued by Clubhouse’s rapid rise that it is now working out how to clone the app, according to a report this month in the New York Times.

And Substack.

Last month the Times also reported that Facebook is developing newsletter tools for reporters and writers. … As with Clubhouse, newsletters hardly pose an existential threat to Facebook. But they do bleed time and attention away from the company’s apps

And Dispo.

Dispo is an invite-only social photo app with a twist: you can’t see any photos you take with the app until 24 hours after you take them. … last month a beta version with social features including shared photo “rolls” launched on iOS, and quickly hit the 10,000-person cap on Apple’s TestFlight software.

And while some of the specific features of these competitive apps may be relatively easy to copy, others won’t be. Here’s Eugene Wei on why Facebook will have a much harder time copying TikTok than it did copying Snapchat:

To clone TikTok, you can't just copy any single feature. It's all of that, and not just the features, but how users deploy them and how the resultant videos interact with each other on the FYP feed. It's replicating all the feedback loops that are built into TikTok's ecosystem, all of which are interconnected. Maybe you can copy some of the atoms, but the magic lives at the molecular level.

TikTok has a a series of flywheels that interconnect, and there isn't any single feature you can copy to recreate the ecosystem. Meanwhile, Reels has to try to compete while being one of like a half dozen things jammed into the Instagram app.

You Can’t Clone Innovation

Like TikTok, the magic of the most successful fintech apps — your Cash Apps3 and Chimes and Affirms — lives at a molecular level. It emerges from the rapid, often chaotic interactions between the companies’ developers, users, and partners. It’s messy and iterative and unpredictable.

It’s not, as much as banks might wish otherwise, a simple list of features that can copied off of a checklist.

It’s hard work and it doesn’t end. Ever.

Digital account opening isn’t a solution that you acquire, install, and then forget about. It’s a set of distinct business processes with different (often conflicting) objectives that require constant tuning in order to achieve the optimal balance. A great digital account opening experiences is the byproduct of continual experimentation and investment.

APIs aren’t, from a technology perspective, new or in any way challenging to build. The challenging part is the ongoing commitment to clearly document them, maintain them over time, and nurture the use of them within your own company and across a diverse ecosystem of external developers. That’s what separates Stripe and Twilio from everyone else.

Machine learning can, to the uninformed observer, appear to be magic, but it’s not:

Under perfect circumstances and fed ideal input data that closely matches its original training data, the resulting solutions are nothing short of magic, allowing their users to suspend disbelief and imagine for a moment that an intelligent silicon being is behind their results. Yet the slightest change of even a single pixel can throw it all into chaos, resulting in absolute gibberish or even life-threatening outcomes.

It’s a powerful, but deeply finicky capability that needs thoughtful parameters and copious training data in order to consistently deliver value.

No Shortcuts

When I was in school, I spent a few years moonlighting as a double bass player in the orchestra. I did fairly well, despite the fact that I never learned how to read sheet music. My trick was glancing over to the bass player to my left (I’m right handed, so my bass was always on my left side) and copying their fingering positions in real time. It worked so well that I climbed up the rankings and even briefly made it to First Chair. The trouble was that, as First Chair, I was suddenly sitting the furthest to the left. There was no longer anyone for me to imitate. It was, predictably, a disaster and I retired as a musician shortly after.

Copying the innovative features of leading fintech apps is a fine short-term strategy. Banks may even be able to improve on some of them (as Facebook argues it improved upon Snapchat’s Stories). Eventually however, the value in such a strategy will be exhausted and banks will need a more sustainable, long-term innovation strategy to fall back on.

Here are a few thoughts on what that long-term strategy should include:

Building new products that address customers’ unmet needs. As I recently wrote about, today’s banks and fintech companies are addressing a vanishingly small percentage of consumers’ total financial needs. The opportunity for new product development in financial services is enormous, but it won’t be realized if every company in financial services keeps copying each other.

Developing equitable partnerships with fintech companies. If you are partnering with a fintech company to get digital account opening capabilities, I have news for you — you aren’t their partner, you’re their client. Banks should strive to do better, which means developing unique value propositions that potential fintech partners will stand to benefit from. Silvergate Bank (a sponsor bank specializing in crypto) and Canapi Ventures (a growth-stage fintech VC firm backed by banks) are instructive examples.

Shipping faster and shipping more. The typical advice to banks competing with fintech companies is to embrace an agile software development methodology and ship constantly. However, as Eugene Wei correctly notes in his article on TikTok, the goal isn’t to ship features but flywheels and flywheels take more work:

Building a flywheel, though, often requires connecting a series of features at once. … If a flywheel requires three or four or even more things to connect in your app, it takes more work to ship all of them at once

Thus, banks’ goal should be to ship both more frequently than they currently do (a low bar) and to be strategic in shipping multiple features that can be assembled in differentiating flywheels.4

Sponsored Content

FINTECH MEETUP is a new event from the founders of MONEY20/20 and SHOPTALK! We’re scheduling 10,000+ 15-minute online meetings so you can meet new people and get business done. Prices go up at midnight on 3/19. Get Ticket Now -- Qualifying Retailers & Merchants/Banks & Credit Unions can join for free! Fintech Meetup is not affiliated with Money20/20 or Shoptalk.

Short Takes

(Sourced from This Week in Fintech)

R&D vs. Innovation Theater

JP Morgan will shut down Chase Pay at the end of the month. The bank also hired HSBC digital partnerships head Jeremy Balkin as head of innovation.

Short take: Simon Taylor has a great overview of the structural challenges that banks like Chase have in driving a good return on their R&D investments (like Chase Pay). These structural challenges make it tempting to focus on “innovation theater” as opposed to actual innovation, which might explain why the man behind Pepper the robot banker is joining Chase as Head of Innovation for Wholesale Payments.

Rewards that Matter

Mastercard partnered with Deserve and Seneca Women to launch a card that rewards users for shopping at women-owned businesses.

Short take: This is a trend I can get behind. Following on the heels of First Boulevard, which rewards cardholders for shopping at black-owned small businesses, Seneca Women is launching a card that rewards customers for shopping at women-owned businesses. More of this please.

The Disturbing Potential of Embedded Finance

It emerged that Apple can disable iCloud, App Store, and Apple ID accounts for users who don’t pay down their credit card bills.

Short take: This is a tiny window into a potentially dystopian future. Everyone in fintech loves the concept of embedded finance, but if a tech platform provider can cut users off from their platform in order to facilitate collection of a delinquent payment on an embedded loan for a product that the platform provider sells… well, let’s just say we’ll long for the days when our biggest complaint was banks’ collection practices.

Alex Johnson is a Director of Fintech Research at Cornerstone Advisors, where he publishes commissioned research reports on fintech trends and advises both established and startup financial technology companies.

Twitter: @AlexH_Johnson

LinkedIn: Linkedin.com/in/alexhjohnson/

Ana Botín’s argument that non-bank technology companies should have to share consumer data (with consumer permission) with banks has merit. After all, it is the customer’s data. For more on this, check out this paper from the Financial Stability Institute.

These banker bylines conveniently ignore the competitive moats that banks have enjoyed over non-bank companies for decades.

Cash App is the closest parallel to TikTok’s flywheel-driven ecosystem. Take a look at their Q4 2020 shareholder letter for more details on the emerging Cash App ecosystem.

Jamie Dimon hit on this need to move faster and deliver more in the same earnings call where he complained about fintech companies’ regulatory advantages. In a response to question from Mike Mayo, he said “we have plenty of resources, a lot of very smart people. We just got to get quicker, better, and faster.”

On a related note: can Netflix or Spotify or someone please convince Jamie Dimon and Mike Mayo to co-star in an unscripted show of some type? I need this more than once a quarter.