Unicorns are Boring

Fintech needs to live by this motto: no problem is too small.

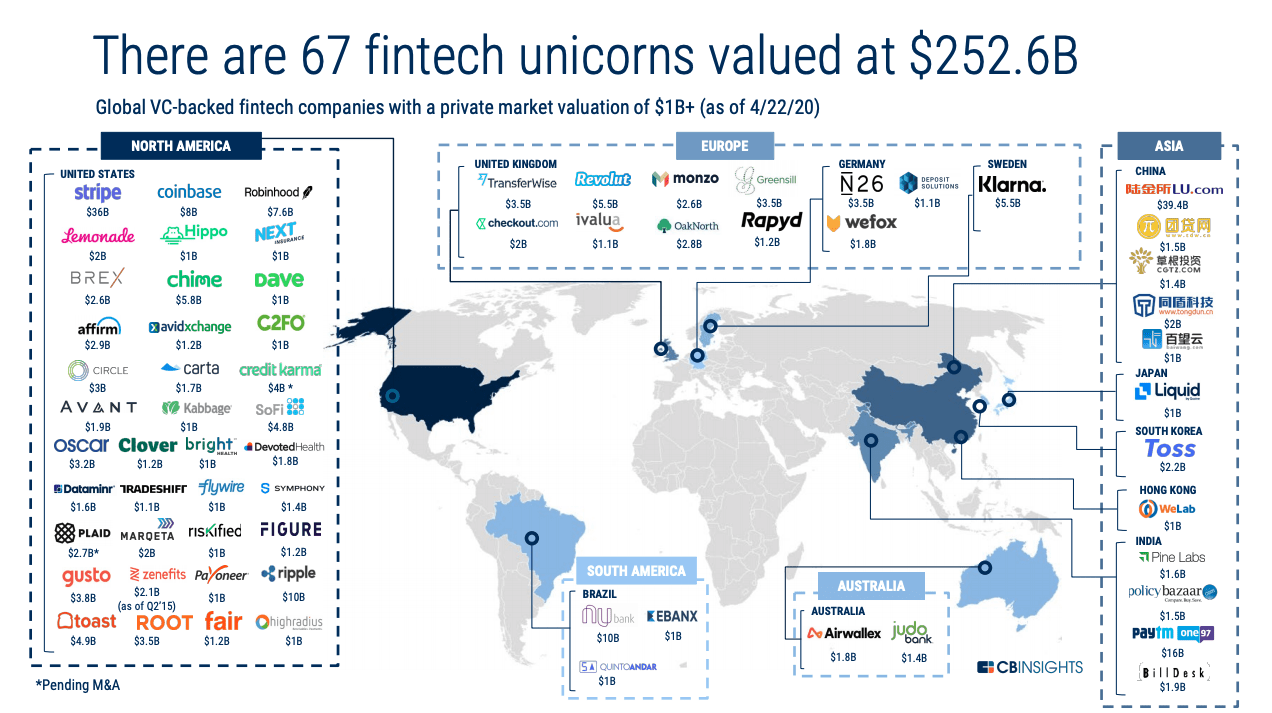

When I look at this graphic:

The first thing I think of is this:

Specifically, I think of these two lines:

Strikeouts are boring! Besides that, they're fascist. Throw some ground balls – it's more democratic.

Let's have some fun out here! This game's fun, OK? Fun goddamnit.

Unicorns in venture capital investing (like strikeouts in baseball) are highly desirable. The reasons for this are obvious and the pursuit of unicorns isn’t necessarily a bad thing. But optimizing everything we do in fintech solely towards the creation of more unicorns is, like a baseball game with no hits, boring and (at some fundamental level) counterproductive.

After all, as Crash Davis reminds us, this game is supposed to be fun.

Larger and Later

Venture capital investments are increasingly becoming concentrated, with a small number of companies raising larger and later rounds:

during our look into United States’ results during the period, we noted that “54% of all venture capital money invested in the United States in the third quarter was part of rounds that were $100 million or more,” with those 88 rounds — a record — totaling $19.8 billion.

The other 1,373 rounds in the quarter had to split the rest of the money. And the percentage of rounds that are late-stage is rising, along with their average deal size, to add to the trend.

This trend can be seen clearly in fintech:

Top-line numbers from PitchBook concerning North American and European venture capital results for fintech in Q3 are as follows: $8.9 billion in total capital raised, +$1.3 billion or +17% from Q2 2020’s $7.6 billion haul.

But, as PitchBook notes, “only 414 deals closed during the quarter—the lowest count since Q3 2017.” More capital then, into fewer rounds. That sounds familiar.

And is perhaps best summarized by this graphic:

I don’t know a single person in fintech (including myself) who wouldn’t LOVE to invest in Stripe, which is great for the Collison brothers as it enables them to continue pursuing their ambitious vision of increasing the GDP of the internet without having to answer to the quarter-to-quarter needs of shareholders.

But I can’t help but wonder what the opportunity costs are of a (rumored) Series G round for Stripe. How else could those hundreds of millions of dollars be spent?

Community Banks are Vital

There are more than 5,000 banks in the U.S. The vast majority of those are small community banks, a remarkable fact that is made even more remarkable when you consider that between 1990 and 2018 the number of banks with assets less than $500 million declined by about 70%, representing a loss of about 7,600 institutions.

This loss has been driven, over the last 30 years, by the shift from a branch-based distribution model to a digital-based one.

With branches, community banks could (for certain products) outmaneuver their larger competitors through personalized person-to-person service and closer ties to the community.

With the shift to digital, community banks’ advantages have disappeared — personalization is now more a function of algorithms than of customer service representatives and community banks haven’t yet figured out how digitize that ephemeral ‘community presence’.

The consolidation of the community banking market isn’t surprising, but it is a problem because community banks are important.

The fact that community banks can’t, by definition, outgrow the communities they serve is an important counterbalance for an industry that often treats people like numbers in a spreadsheet.

Take the Paycheck Protection Program as an example:

Banks hold the vast majority of the $525 billion in PPP loans made by banks and nonbanks. Community banks’ participation in the PPP outpaced noncommunity banks. As of June 30, 2020, banks held $482 billion, or 92 percent of total PPP loans. Community banks held $148 billion—28 percent of total PPP loans and 31 percent of PPP loans held by banks. This share is significant, as community banks held 12 percent of total industry assets and 15 percent of total industry loans as of June 30, 2020.

When you strip financial services back to its most fundamental and important jobs, it’s difficult to make the case that smaller companies intently focused on the needs of specific customer segments aren’t vitally important.

The Long Tail of Banking

The good news is that the internet specializes in efficiently and cost-effectively connecting niche customer segments with providers offering the exact things those customers are looking for.

Here’s Chris Anderson (writing about the entertainment industry):

For too long we've been suffering the tyranny of lowest-common-denominator fare, subjected to brain-dead summer blockbusters and manufactured pop. Why? Economics. Many of our assumptions about popular taste are actually artifacts of poor supply-and-demand matching—a market response to inefficient distribution. … This is the world of scarcity. Now, with online distribution and retail, we are entering a world of abundance. And the differences are profound.

The same ‘long tail’ effect applies in financial services. Customer segments with unique financial services needs can, for the first time in history, efficiently find and purchase from financial services providers that specialize in meeting those exact needs.

But how unique can those needs really be? Isn’t banking basically the same for everybody?

Major banks have rolled out initiatives that allow customers to use their preferred name on their cards, but as Daylight’s cofounder and chief of staff Billie Simmons can attest to personally, that’s not always enough. “Some of my credit cards, I just never updated my name, because it was such a complex and difficult process,” says Simmons, who describes herself as a proud transwoman. “My checking account, I have updated my name and gender legally, but one thing I can’t do is update my username. So every time I log in, I have to dead-name myself. … So a name on a card is a good start, but actually this stuff runs deeper. We often talk about no problem is too small, because those are the things that we’re spending our time on.

“No problem is too small”. That’s a critical difference between neobanks like Daylight and traditional banks. It’s also a critical difference between community-focused neobanks and every other neobank.

The standard neobank playbook is to find a wedge — refi loans for student debt, higher savings rates in a low-rate environment, eliminating overdraft fees — to attract an initial base of customers and then build out (new products to cross-sell) and up (growing beyond the initial target customer segment).

There’s absolutely nothing wrong with this. These neobanks are attacking value deficits and forcing large market incumbents to adapt, usually to the benefit of customers. That’s a good thing.

But most neobanks are trying to become the next JPMorgan Chase.

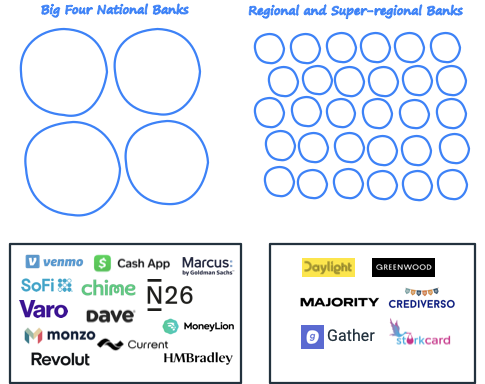

We also need neobanks that are trying to become the next KeyBank (my personal most interesting regional bank) and the next Centier Bank (a small community bank based in Indiana that I just picked out of a hat).

Good news — we’re starting to get some!

Daylight (referenced above) is built by and for the LGBT+ community. Majority, the first “financial membership” built by and for migrants. Greenwood, a digital banking platform for Black and Latinx people and business owners. Crediverso, an online financial products marketplace built for the US Latino community. Gather, a digital bank account for couples. And StorkCard, a digital banking app for new parents.

Simon Taylor at 11:FS has a great newsletter on why big banks struggle to serve these communities, which he terms “massive niches”.

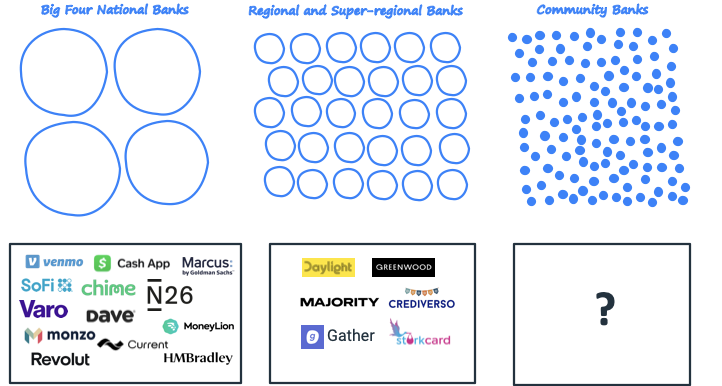

I love that term. It perfectly describes the layer of opportunity that sits below the big national banks (and the neobanks trying to replace them). It is, in some ways, analogous to the regional and super-regional banking market that we have today.

The other reason I love the term “massive niches” is that it begs a really interesting follow-up question — what about the less-than-massive niches?

In theory, a company should be able to profitably deliver digital banking products through digital banking channels to even smaller communities than the ones named above.

What does that look like? Is there a compelling product offering at that level? How granular can we get and still deliver significant value?

To use StorkCard as an example (because it’s a community I have lived experience in), are the differences between different types of parents — married and both working, married with one working and one staying home, divorced and both working, etc. — meaningful enough to justify distinct banking products?

In a world with branches and a large number of humans staffing them, definitely not.

In a world with digital apps and a robust banking-as-a-service infrastructure to build upon, maybe?

This is the question that I’d like to have answered — what does the digital equivalent to a small community bank look like?

I’m a little worried I may never find out.

At a certain point, digital community banks stop making sense to invest in if the investors evaluating it only care about reaching that magical $1B valuation.

I believe digital community banks can become a category of profitable, durable businesses that solve real pain points. The question is will they be given a chance to prove it?

Short Takes

(Sourced from This Week in Fintech and paying homage to Bull Durham)

“Bad trades are a part of baseball”

Ant Group is in more hot water in China, as bank partners claim that they became dependent on the platform for loan issuance, but were then left to manage defaults on their own due to high-risk originations.

Short take: When bank executives have nightmares about the future of Banking-as-a-Service, this is exactly what they dream about.

“I’m just happy to be here. Hope I can help the ball club.”

OneBanks, a fintech startup looking to bring full-service banking kiosks to places banks have abandoned, is looking to pilot in the Scottish town of Denny.

Short take: A blindspot for fintech founders and product managers is assuming everyone is like them, which (at the most fundamental level) means owning a smartphone and living on the internet. In reality, not everyone has access to the internet nor owns a smartphone. Banking deserts are real. It’s nice to see a fintech startup solving for them.

“I’m the player to be named later”

Synctera came out of stealth to debut a fintech and community bank matchmaking platform.

Short take: I had been wondering what Peter Hazlehurst (former Head of Uber Money) was going to do next. This is a good one. The reason I think we need a new generation of digital community banks is because I’m skeptical that the current generation can catch up. Synctera may help prove me wrong.

Thanks,

Alex Johnson